Pipeline & Process Services Market Size

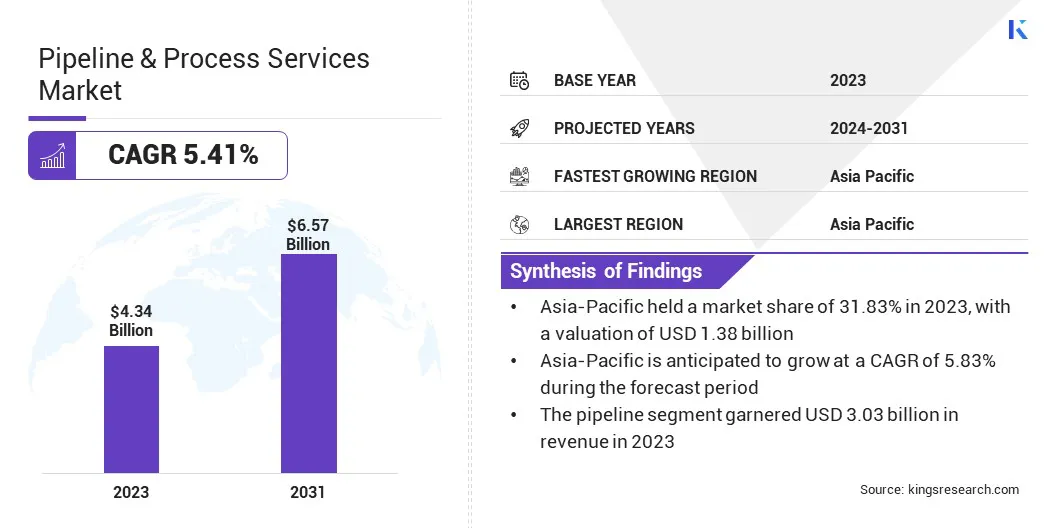

The Global Pipeline & Process Services Market size was valued at USD 4.34 billion in 2023 and is projected to grow from USD 4.55 billion in 2024 to USD 6.57 billion by 2031, exhibiting a CAGR of 5.41% during the forecast period.

The increasing global energy demand, particularly in emerging economies, highlights the need for expanded transportation and processing infrastructure. As sectors such as transportation, manufacturing, and power generation increase their oil and gas consumption, the demand for pipeline construction, maintenance, and process services grows.

In the scope of work, the report includes products and services offered by companies such as Halliburton Energy Services, Inc., Baker Hughes Company, EnerMech, TechnipFMC plc, Trans Asia Pipeline Services, Ideh Pouyan Energy Co., STEP ENERGY SERVICES, Chenergy Services Limited, STATS Group, Hydratight, and others.

The pipeline & process services market plays a critical role in the energy industry, enabling the efficient and safe transportation and processing of hydrocarbons. This market is characterized by ongoing technological innovation, with companies focusing on improving operational efficiency, safety, and environmental compliance.

As energy needs evolve, there is an increasing demand for advanced solutions that optimize pipeline performance, enhance processing capabilities, and meet stricter regulatory standards, particularly in complex and high-risk environments.

- As per the OPEC Annual Report of 2023, OPEC crude oil production averaged 27.0 mb/d, underscoring the increasing demand for pipeline and process services infrastructure to support the transportation and processing of rising hydrocarbon production.

The market involves activities related to the construction, maintenance, and operation of pipelines and processing facilities in the energy industry. This market includes services that ensure the efficient and safe transportation of hydrocarbons, as well as the processing of raw oil and gas into usable products.

The market covers pipeline installation, inspection, cleaning, and repairs, as well as services to optimize refining, treatment, and separation processes. These services are essential for maintaining infrastructure integrity and ensuring smooth oil and gas flow from extraction sites to refineries or distribution points while meeting regulatory and safety standards. The market plays a crucial role in supporting the global energy supply chain.

Analyst’s Review

Companies in the pipeline & process services market are increasingly focusing on strategic partnerships and collaborations to secure large-scale infrastructure projects, particularly in developing regions. To maintain competitiveness, they are investing in advanced technologies for pipeline construction, optimization, and maintenance, ensuring higher efficiency and reliability.

- In October 2024, Enterprise Products Partners L.P. acquired Piñon Midstream for USD 950 million, expanding its footprint in the Delaware Basin. This acquisition aligns with the company’s strategy of securing large-scale infrastructure projects and investing in advanced technologies.

Additionally, several companies are adopting innovative project management strategies to enhance service delivery, focusing on comprehensive solutions that cover planning, design, construction, and ongoing maintenance. This approach helps them meet the complex needs of expanding infrastructure while ensuring safety and compliance.

- In December 2024, Saipem was awarded the final contract for the Northern Endurance Partnership (NEP) and Net Zero Teesside Power (NZT) projects, valued at USD 678 million. These offshore projects aim to support the UK’s Net Zero objectives by facilitating CO2 transportation and storage. Saipem will manage the EPCI of pipelines and water outfalls, contributing to zero-emission targets.

Pipeline & Process Services Market Growth Factors

Pipeline & Process Services Market Growth Factors

Technological advancements are transforming the pipeline & process services industry by enhancing efficiency, safety, and reliability. Innovations in process control systems, automation, and optimization services help streamline operations, reduce downtime, and ensure smoother workflows.

Additionally, the introduction of advanced pipeline monitoring technologies, such as real-time monitoring and predictive maintenance, allows for early detection of issues, minimizing risks and operational costs. These advancements are fueling growth by enabling more effective management of complex pipeline systems and improving overall service delivery.

- In April 2024, Louisiana State University introduced a breakthrough in pipeline leak detection, using fiber optics and advanced signal processing algorithms. This technology enables real-time, accurate leak detection, reducing environmental damage and repair costs. It can be installed along pipelines, enhancing safety, efficiency, and minimizing false alarms for oil and gas companies.

Regulatory compliance poses a significant challenge to the development of the pipeline & process services market due to constantly evolving environmental, safety, and operational regulations across regions.

To address this challenge, companies are increasingly investing in specialized legal and compliance teams, along with advanced monitoring systems. Additionally, proactive employee training and the adoption of standardized best practices help ensure consistent adherence to regional laws, reducing risks and enhancing operational efficiency while ensuring safety and environmental responsibility.

Pipeline & Process Services Industry Trends

The market is increasingly focused on sustainability and decarbonization to support global greenhouse gas reduction efforts.

Key trends include expanding pipeline infrastructure for Carbon Capture and Storage (CCS) to transport captured CO2, the development of hydrogen transport pipelines as a cleaner fuel alternative, and the adoption of advanced leak detection technologies such as fiber optics and acoustic sensors to ensure pipeline integrity and minimize environmental risks. These initiatives are critical to achieving climate goals.

- As of December 2024, the Northern Lights project, a joint venture between TotalEnergies, Equinor, and Shell, marks a significant milestone in CO2 transport and sequestration, with a capacity to store 1.5 million tons of CO2 annually. This reflects the growing trend of sustainability in the market.

Another key trend in the pipeline & process services market is the energy transition, supported by the shift to renewable energy sources. Pipelines originally designed for fossil fuels are being adapted to transport biofuels, natural gas, and green hydrogen.

Hybrid pipelines, capable of carrying both traditional and renewable fuels, are optimizing existing infrastructure. Additionally, with the growth of wind and solar energy, energy storage solutions such as compressed air and pumped storage are utilizing pipelines for efficient transport.

- In October 2024, Eni secured UK government funding for the Liverpool Bay CO2 transport and storage project, marking a significant milestone for the HyNet initiative. This project is part of a broader effort supported by the UK government, which has committed USD 27.30 billion in funding over the next 25 years to advance carbon capture and storage technologies, furthering the country’s efforts to reduce carbon emissions and transition to a low-carbon economy.

Segmentation Analysis

The global market has been segmented based on asset, operation, location, and geography.

By Asset

Based on asset, the market has been segmented into pipeline and process. The pipeline segment led the pipeline & process services market in 2023, reaching a valuation of USD 3.03 billion. This notable expansion is largely attributed to rising global demand for energy, oil, and gas.

As industries focus on efficient and reliable transportation of resources, investments in pipeline infrastructure have surged. Technological advancements in pipeline construction, inspection, and maintenance have improved operational efficiency, thus driving segmental growth.

Furthermore, the increasing emphasis on cleaner energy, including natural gas, is leading to the expansion of pipeline networks. This shift, along with the growth of renewable energy projects requiring integrated transportation systems, creates lucrative opportunities that is fueling the expansion of the segment.

By Operation

Based on operation, the market has been classified into pre-commissioning and commissioning, maintenance, inspection, and decommissioning. The maintenance segment secured the largest revenue share of 32.01% in 2023, primarily due to the increasing need for safe and efficient operations in pipeline and process systems.

Aging infrastructure requires regular upkeep to ensure optimal performance, creating a robust demand for maintenance services. Additionally, the rising complexity of high-capacity pipelines and strict regulatory standards necessitate frequent inspections and maintenance to prevent disruptions and ensure safety.

Technological advancements further enhance service efficiency, reducing downtime and maintenance costs. With the expansion of global energy infrastructure and industrial processes, there is a pressing need for specialized maintenance services, thereby propelling segmental growth.

By Location

Based on location, the market has been bifurcated into onshore and offshore. The offshore segment is set to experience significant growth, registering a CAGR of 6.68% through the forecast period. The growing need for efficient transportation and processing of oil, gas, and renewable energy resources from offshore fields is contributing significantly to this growth.

The demand for specialized offshore infrastructure, such as subsea pipelines, platforms, and storage systems, is generating the demand for advanced pipeline and process services. Technological innovations in offshore construction, maintenance, and inspection services are enhancing safety and efficiency. Moreover, the expansion of offshore energy projects is boosting the demand for integrated pipeline and process services.

- In December 2024, Equinor UK Ltd and Shell U.K. Limited formed a joint venture to combine their UK offshore oil and gas assets, establishing the North Sea’s largest independent producer. This partnership aims to sustain the UK’s energy supply, maximize asset value, and drive investment in offshore infrastructure, including pipeline and process services.

Pipeline & Process Services Market Regional Analysis

Based on region, the global market has been classified into North America, Europe, Asia-Pacific, MEA, and Latin America.

The Asia-Pacific pipeline & process services market accounted for a substantial share of around 31.83% in 2023, with a valuation of USD 1.38 billion. This dominance is reinforced by the region’s rapid industrialization, significant energy demand, and large-scale infrastructure development.

The Asia-Pacific pipeline & process services market accounted for a substantial share of around 31.83% in 2023, with a valuation of USD 1.38 billion. This dominance is reinforced by the region’s rapid industrialization, significant energy demand, and large-scale infrastructure development.

Countries such as China, India, and Japan are investing heavily in energy and natural gas pipelines to support economic growth and energy security. The region is a key hub for oil and gas exploration, with numerous offshore and onshore projects requiring specialized pipeline services.

Additionally, the shift toward cleaner energy sources, such as natural gas and renewables, has highlighted the need for pipeline and process services, positioning it as a major market.

North America pipeline & process services market is projected to witness significant growth over the forecast period, recording a CAGR of 5.45%. This rapid growth Is propelled by its vast oil, gas, and renewable energy reserves. The U.S. and Canada are major contributors to pipeline infrastructure development, supporting both traditional energy and expanding natural gas markets.

Increased oil production, coupled with substantial investments in energy transport and storage, has created a strong demand for pipeline services. Additionally, the transition to cleaner energy sources and carbon capture technologies fosters regional market growth. Technological advancements and strong regulatory frameworks continue to support robust expansion in pipeline and process services across North America.

Competitive Landscape

The global pipeline & process services market report will provide valuable insight with an emphasis on the fragmented nature of the industry. Prominent players are focusing on several key business strategies such as partnerships, mergers and acquisitions, product innovations, and joint ventures to expand their product portfolio and increase their market shares across different regions.

Investments in research and development, the establishment of new manufacturing plants, and improvements in supply chain efficiency could present new growth opportunities in the market.

List of Key Companies in Pipeline & Process Services Market

- Halliburton Energy Services, Inc.

- Baker Hughes Company

- EnerMech

- TechnipFMC plc

- Trans Asia Pipeline Services

- Ideh Pouyan Energy Co.

- STEP ENERGY SERVICES

- Chenergy Services Limited

- STATS Group

- Hydratight

Key Industry Developments

- March 2023 (Partnership): ABB India partnered with Numaligarh Refinery Ltd to provide integrated automation and control solutions for the 130 km India-Bangladesh cross-border oil pipeline. The project features ABB Ability SCADAvantage, Remote Terminal Units (RTUs), and a leak detection system to monitor pipeline performance, ensuring safety and efficiency. The system offers real-time data access, optimizing operations and supporting Bangladesh's growing energy demand by securely transporting diesel from India.

The global pipeline & process services market has been segmented as:

By Asset

- Pipeline

- Transmission

- Distribution

- Process

- Refinery & Petrochemical

- Gas Processing

- Gas Storage

By Operation

- Pre-commissioning and Commissioning

- Maintenance

- Inspection

- Decommissioning

By Location

By Region

- North America

- Europe

- France

- UK

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America