Offshore Wind Energy Market Size

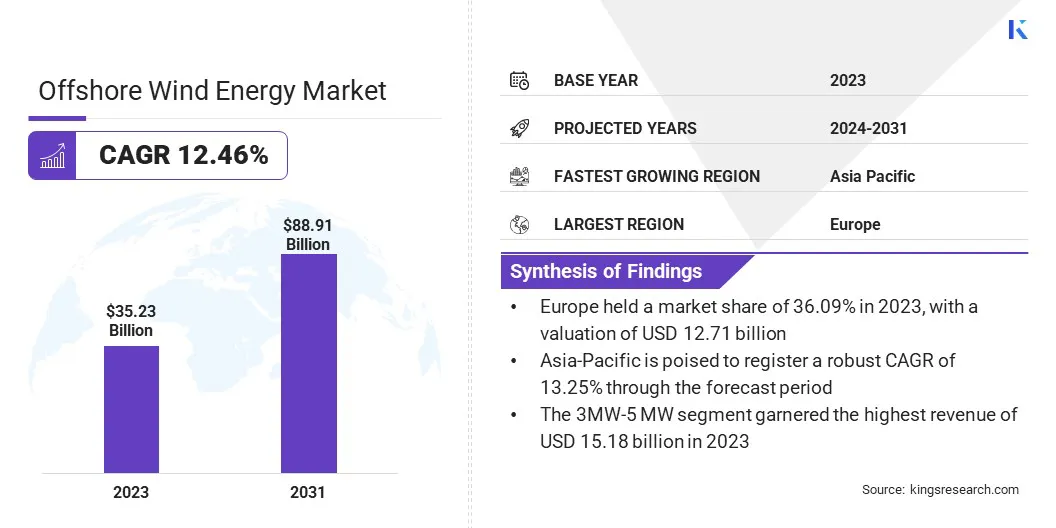

Global Offshore Wind Energy Market size was recorded at USD 35.23 billion in 2023, which is estimated to be at USD 39.07 billion in 2024 and projected to reach USD 88.91 billion by 2031, growing at a CAGR of 12.46% from 2024 to 2031. In the scope of work, the report includes services offered by companies such as General Electric, Equinor ASA, Iberdrola, S.A., Mitsubishi Heavy Industries, Ltd, Goldwind, Naval Group, Nordex SE, Siemens, ABB, MODEC, Inc., and others.

The growth of floating wind farms represents a significant evolution in the offshore wind energy market. Technological advancements in floating platform designs, such as semi-submersible and spar-buoy configurations, have played a crucial role in this growth. Moreover, floating wind farms have the potential to reduce visual and noise impacts on coastal communities, addressing some environmental and social concerns associated with nearshore wind farms.

A key driver behind the expansion of floating wind farms is the increasing demand for renewable energy sources, driven by global efforts to combat climate change. Government incentives and research funding are also bolstering the sector, as policymakers recognize the need to diversify energy portfolios and enhance energy security. With continuous innovation and scaling, floating wind farms are poised to become a major contributor to the global energy mix.

Offshore wind energy refers to the generation of electricity by harnessing the wind's power over open bodies of water, typically oceans or large lakes. This type of energy production utilizes wind turbines that are specifically designed to operate in marine environments. The main components of offshore wind turbines include the rotor (comprising the blades and hub), the nacelle (which houses the generator, gearbox, and other critical components), and the tower.

Additionally, offshore wind farms require robust foundation structures, such as monopiles, jackets, or floating platforms, to support the turbines. These installations are located away from the shore, often several kilometers out to sea, where wind speeds are generally higher and more stable than on land.

- Offshore wind farms can vary greatly in capacity, with some projects exceeding 1,000 megawatts (MW), capable of powering hundreds of thousands of homes.

The strategic placement of these turbines in high-wind areas, combined with their large sizes, allows for substantial electricity generation, making offshore wind a vital component of the renewable energy landscape.

Analyst’s Review

The offshore wind energy market is witnessing rapid growth and transformation, driven by technological advancements, favorable regulatory frameworks, and increasing investment in renewable energy infrastructure. As the market expands, key players are adopting a variety of strategies to maintain competitiveness and capitalize on emerging opportunities.

Companies are investing in the development of larger and more efficient turbines, which can generate more power per unit and reduce overall costs. Innovations such as floating wind platforms are also enabling access to deeper waters with stronger wind resources.

- For instance, in June 2024, Qualitas Energy, a global platform specializing in renewable energy, energy transition, and sustainable infrastructure investment, announced the successful acquisition of a repowering project in Brandenburg, Germany, with a development potential of 36 MW.

Furthermore, market leaders are focusing on securing long-term power purchase agreements (PPAs) with corporate and utility customers, providing stable revenue streams and reducing financial risks. Strategic partnerships and collaborations are becoming increasingly important, as companies seek to pool resources and expertise to undertake large-scale projects.

Additionally, expanding into emerging markets with untapped offshore wind potential is a key growth strategy. These markets often offer favorable conditions, such as supportive government policies and high demand for clean energy.

- For instance, in May 2024, METEORAGE and RECASE signed an agreement to enhance wind energy solutions in Germany, offering users access to cutting-edge technology, proven global expertise, and highly accurate data.

Offshore Wind Energy Market Growth Factors

The rising demand for renewable energy is a pivotal driver shaping the offshore wind energy market. With growing concerns about climate change and environmental sustainability, governments, businesses, and consumers are increasingly prioritizing clean energy sources. Renewable energy, including offshore wind, offers a viable solution to reduce greenhouse gas emissions and mitigate the impacts of climate change.

This increased demand is driven by various factors, including international commitments to reduce carbon emissions, such as the Paris Agreement, as well as increasing public awareness of the environmental and health benefits of renewable energy. Moreover, advancements in technology have led to significant cost reductions in renewable energy generation, making it increasingly competitive with conventional fossil fuels.

- For instance, in January 2024, TotalEnergies signed an agreement with European Energy to develop offshore wind projects in Denmark, Finland, and Sweden. This includes acquiring an 85% stake in Denmark’s Jammerland Bugt project (240 MW) and a 72.2% stake in Lillebaelt South (165 MW). These projects obtained exclusivity and grid connection permits, with construction permits expected by mid-2024 and operations starting by 2030.

One of the significant challenges facing the offshore wind energy market is the high initial capital investment required for project development and installation. Unlike onshore wind farms, offshore installations involve complex engineering, construction, and logistical challenges that drive up costs significantly.

The development of offshore wind farms requires substantial upfront investment in site surveys, environmental assessments, permitting processes, and the construction of offshore infrastructure, such as foundations and subsea cabling.

Additionally, the offshore environment introduces additional risks and uncertainties, such as harsh weather conditions and challenging seabed conditions, which can further escalate project costs. This high capital requirement can deter potential investors and developers, particularly in regions where regulatory frameworks are not well-established or where access to financing is limited.

Overcoming this challenge requires innovative financing mechanisms, such as public-private partnerships, government subsidies, and financial incentives, to mitigate investment risks and attract capital to the sector.

Offshore Wind Energy Market Trends

Advancements in subsea technology are driving significant improvements in the offshore wind energy sector. Subsea technology encompasses a range of innovations, including underwater cabling, monitoring systems, and maintenance equipment, designed to enhance the efficiency, reliability, and lifespan of offshore wind infrastructure.

One key area of advancement is subsea cabling, where developments in cable design and installation techniques have enabled longer cable runs and higher transmission capacities, reducing energy losses and lowering overall project costs.

Additionally, the integration of advanced monitoring and control systems allows for real-time performance monitoring and predictive maintenance, optimizing operational efficiency and minimizing downtime. These advancements are crucial for the scalability and long-term viability of offshore wind farms, particularly as the industry continues to expand into deeper waters and more challenging environments.

Furthermore, ongoing research and development in subsea technology are expected to further drive down costs and improve the overall competitiveness of offshore wind energy in the global energy market.

Segmentation Analysis

The global market is segmented based on component, location, capacity, and geography.

By Component

Based on component, the market is categorized into turbine, electrical infrastructure, and substructure. The turbine segment captured the largest offshore wind energy market share of 46.35% in 2023. Turbines are responsible for converting the kinetic energy of the wind into electrical power, which makes them essential for offshore wind farms.

- In 2023, the turbine segment dominated the market primarily due to the increasing deployment of larger and more efficient turbines.

Technological advancements have led to the development of turbines with higher capacities and improved performance, allowing for greater energy production per turbine. Additionally, economies of scale have driven down the cost of turbine manufacturing and installation, making offshore wind energy more cost-effective compared to other renewable energy sources.

By Location

Based on location, the offshore wind energy market is classified into shallow water, transitional water, and deep water. The shallow water segment is poised to record at a staggering CAGR of 13.87% through the forecast period. Shallow water sites, typically located close to the shore, offer several advantages for offshore wind development.

Firstly, the installation and maintenance of turbines in shallow waters are more straightforward and less costly compared to deeper waters, as they require less complex foundation structures and installation methods.

Secondly, shallow water sites often benefit from higher wind speeds and more favorable ocean conditions, leading to increased energy production and operational efficiency. Additionally, regulatory frameworks and government incentives are favoring the development of shallow water projects, providing further impetus for growth.

By Capacity

Based on capacity, the offshore wind energy market is divided into up to 3 MW, 3MW - 5 MW, and above 5 MW. The 3MW - 5 MW segment garnered the highest revenue of USD 15.18 billion in 2023 propelled by the widespread adoption of mid-sized turbines in offshore wind projects. Turbines in the 3MW - 5 MW range are considered to have a balance between power output, cost-effectiveness, and technological maturity.

In 2023, this segment witnessed the highest revenue due to several factors. Firstly, mid-sized turbines offer a good balance between energy production and project economics, making them attractive for developers seeking to maximize returns on investment.

Secondly, technological advancements have improved the efficiency and reliability of mid-sized turbines, reducing operational costs and enhancing performance. Additionally, government policies and market dynamics may favor the deployment of mid-sized turbines, further driving demand in this segment.

Offshore Wind Energy Market Regional Analysis

Based on region, the global market is classified into North America, Europe, Asia-Pacific, MEA, and Latin America.

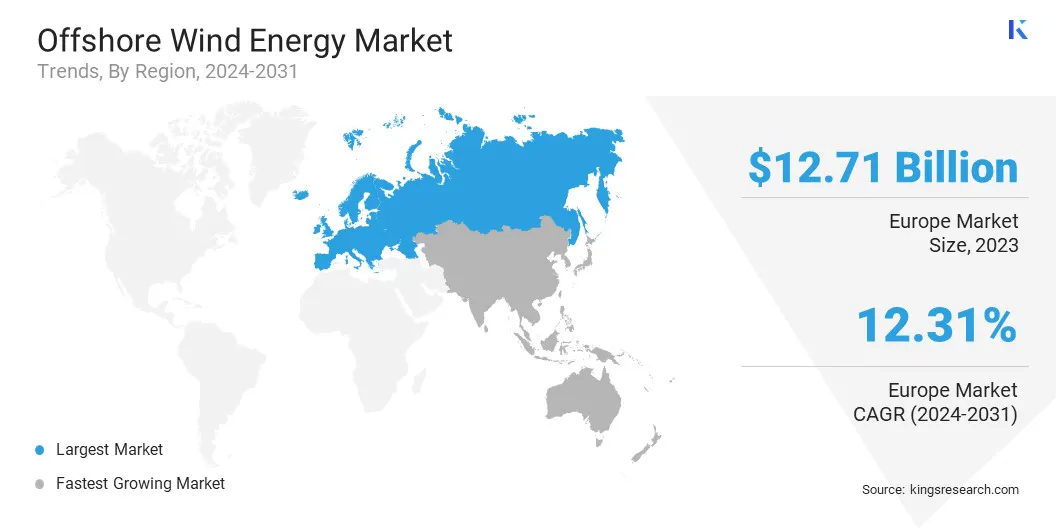

The Europe Offshore Wind Energy Market share stood around 36.09% in 2023 in the global market, with a valuation of USD 12.71 billion, reflecting the region's prominent position in the global market. Europe has been at the forefront of offshore wind development for several decades, with countries like the United Kingdom, Germany, and Denmark leading the way in project installations and technological innovation.

Favorable regulatory frameworks, ambitious renewable energy targets, and strong government support have created a conducive environment for offshore wind investment and development in Europe.

- For instance, in March 2024, WindEurope and the Azerbaijan Renewable Energy Agency signed an MoU to promote onshore and offshore wind energy in Azerbaijan and the Caspian Sea region. This collaboration aims to leverage the area's wind potential, supporting the global goal to triple renewable capacity by 2030.

Additionally, the continent benefits from extensive maritime infrastructure, including ports and supply chains, facilitating the construction and maintenance of offshore wind farms. Furthermore, Europe's experience in offshore engineering and grid integration enables efficient project execution and grid connectivity

Asia-Pacific is poised to grow at the highest CAGR of 13.25% in the forthcoming years, signaling significant opportunities for offshore wind energy expansion in the region.

Countries in Asia-Pacific, including China, Japan, South Korea, and Taiwan, are increasingly turning to offshore wind as a key component of their energy transition strategies to reduce reliance on fossil fuels and combat air pollution. These nations possess vast coastlines and strong wind resources, providing ample opportunities for offshore wind development.

Supportive government policies and incentives, coupled with declining costs of offshore wind technology, are encouraging investment in the sector. Governments are setting ambitious renewable energy targets and implementing measures to streamline permitting processes and facilitate project financing. Additionally, collaborations with international companies and expertise transfer are accelerating the development of Asia-Pacific's offshore wind industry.

Competitive Landscape

The offshore wind energy market report will provide valuable insight with an emphasis on the fragmented nature of the industry. Prominent players are focusing on several key business strategies such as partnerships, mergers and acquisitions, product innovations, and joint ventures to expand their product portfolio and increase their market shares across different regions.

Manufacturers are adopting a range of strategic initiatives, including investments in R&D activities, the establishment of new manufacturing facilities, and supply chain optimization, to strengthen their market standing.

List of Key Companies in Offshore Wind Energy Market

- General Electric

- Equinor ASA

- Iberdrola, S.A.

- Mitsubishi Heavy Industries, Ltd

- Goldwind

- Naval Group

- Nordex SE

- Siemens

- ABB

- MODEC, Inc.

Key Industry Developments

- April 2024 (Expansion): EDF Renewables (South Africa) commissioned the Nordex Group for two wind projects within the Koruson 2 cluster, developed with Anglo American via Envusa Energy. The cluster, including Umsobomvu, Hartebeesthoek wind farms, and Mooi Plants solar farm, will generate 520 MW, with Pele Green Energy and a local community trust holding a 20% equity stake.

- July 2023 (Development): Iberdrola’s first French offshore wind farm, Saint-Brieuc, supplies electricity to the grid, marking its fourth European offshore project. This commissioning strengthened Iberdrola's leadership in offshore wind, with the first green megawatts integrated into the French national electricity grid.

- February 2023 (Partnership): Siemens Gamesa and Doosan Enerbility signed a binding framework agreement for a strategic partnership in South Korea's offshore wind market. This agreement aimed to establish robust local content offerings, which was dependent on securing successful offshore wind power orders in South Korea.

The Global Offshore Wind Energy Market is Segmented as:

By Component

- Turbine

- Electrical Infrastructure

- Substructure

By Location

- Shallow Water

- Transitional Water

- Deep Water

By Capacity

- Up to 3 MW

- 3MW - 5 MW

- Above 5 MW

By Region

- North America

- Europe

- France

- UK

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America