Industrial Distribution Market Size

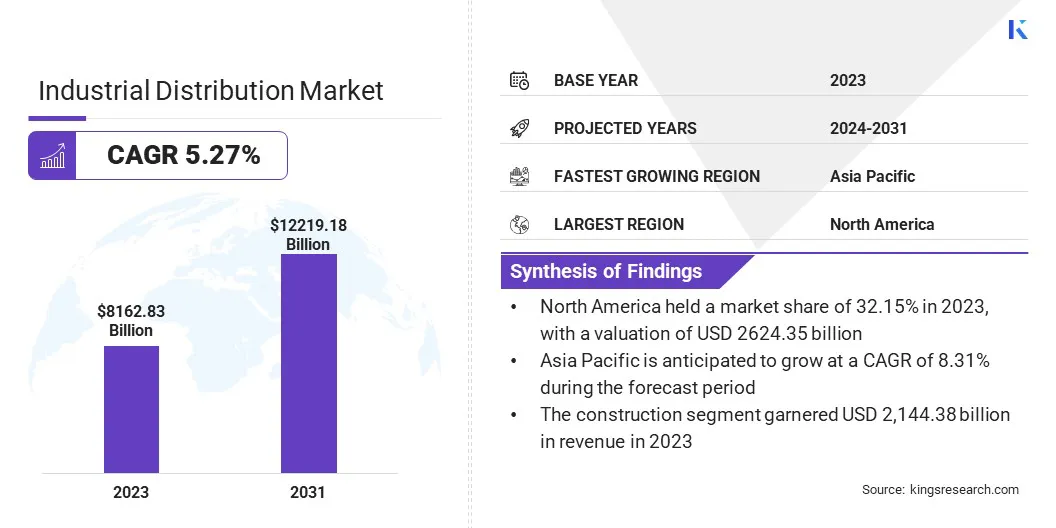

The global Industrial Distribution Market size was valued at USD 8,162.83 billion in 2023 and is projected to reach USD 12,219.18 billion by 2031, growing at a CAGR of 5.27% from 2024 to 2031. In the scope of work, the report includes solutions offered by companies such as Grainger, MSC Industrial Direct Co., Inc., Fastenal Company, Wurth Group, Ferguson plc, WESCO International, Inc., Rexel, HD Supply Holdings, Inc., Sonepar, Wolseley plc, and Others.

The growth of the industrial distribution industry has been significantly shaped by ongoing technological advancements in recent years. Continued progress in automation, the Internet of Things (IoT), and artificial intelligence (AI) played pivotal roles in driving efficiency improvements and cost savings throughout distribution processes. These technologies enabled industrial distributors to optimize inventory management, streamline logistics operations, and enhance customer experiences.

The industrial distribution market is poised to further adopt new technologies to remain competitive and meet evolving customer demands in the foreseeable future. This includes the integration of advanced analytics for predictive maintenance, the deployment of autonomous vehicles for warehouse management, and the implementation of AI-powered algorithms for demand forecasting. Adopting these innovations is likely to drive greater efficiency and productivity while paving the way for more agile and resilient industrial distribution networks in the upcoming years.

Analyst’s Review

The industrial distribution market is set to undergo a profound evolution in the forthcoming years, fueled by the adoption of new technologies. The integration of Industry 4.0 technologies, such as robotics, 3D printing, and blockchain, is poised to revolutionize supply chain management practices. These integrations may enable greater automation, customization, and traceability of products throughout the distribution process, enhancing the efficiency and operational capabilities.

Moreover, the increasing adoption of circular economy principles might require industrial distributors to prioritize resource efficiency, product lifecycle management, and waste reduction. This may lead to the development of closed-loop supply chains and sustainable business practices, aligning with environmental objectives while enhancing profitability.

Additionally, the shift toward predictive maintenance models and servitization is set to transform traditional business models, as industrial distributors offer value-added services such as maintenance, repairs, and equipment leasing alongside product sales. This shift is likely to optimize asset utilization while fostering stronger customer relationships. Overall, these trends signify a dynamic and transformative trajectory for the industrial distribution industry in the upcoming years.

Market Definition

Industrial distribution refers to the process of sourcing, purchasing, storing, and delivering products and materials necessary for the functioning of industrial operations across various industries. It encompasses a wide range of activities, including procurement, inventory management, logistics, and customer service, aimed at ensuring the timely and efficient supply of goods to industrial customers.

The application areas of industrial distribution are diverse, spanning across industries such as manufacturing, construction, energy, healthcare, automotive, aerospace, and others. In manufacturing, industrial distributors play a critical role in supplying raw materials, components, and equipment needed for production processes. In construction, they provide building materials, tools, and equipment to contractors and builders.

In energy, they supply parts and components for infrastructure maintenance and operations. Overall, industrial distribution facilitates the flow of goods from manufacturers to end-users, thereby supporting the smooth operation of industrial activities. Industrial distribution is subject to various laws and regulations that govern various aspects such as product safety, environmental protection, transportation, and trade.

- For instance, in the US, industrial distributors must comply with regulations set by agencies such as the Occupational Safety and Health Administration (OSHA) for workplace safety and the Environmental Protection Agency (EPA) for environmental compliance.

Similarly, within the European Union, industrial distribution adheres to regulations such as REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals) ensuring the safe handling of chemicals, and RoHS (Restriction of Hazardous Substances) limiting hazardous substances in electrical and electronic equipment. Industrial distributors must maintain rigorous standards of quality and safety across their operations to comply with these regulations.

Industrial Distribution Market Dynamics

The growing demand for just-in-time (JIT) delivery solutions is a significant driver propelling the growth of the industrial distribution sector. JIT delivery involves supplying products and materials to customers precisely when they are needed, thereby minimizing inventory holding costs and streamlining operations. Businesses are increasingly adopting lean manufacturing practices, which emphasize efficiency and waste reduction, making JIT delivery an attractive option to minimize excess inventory and associated costs.

Moreover, the rise of e-commerce and omnichannel retail has increased customer expectations for faster and more reliable delivery, prompting industrial distributors to optimize their supply chains to meet these demands. Additionally, globalization and the expansion of international trade have led to more complex supply chains, increasing the need for JIT delivery solutions to ensure timely and efficient delivery of goods across borders.

On the other hand, supply chain disruptions impede the growth of the industrial distribution market. These disruptions arise from a variety of events, including natural disasters such as earthquakes, hurricanes, or floods, which damage infrastructure, disrupt transportation networks, and interrupt production. Furthermore, geopolitical tensions, trade disputes, and regulatory changes disrupt supply chains by imposing tariffs, trade barriers, or export restrictions, leading to delays and increased costs for importing or exporting goods.

These disruptions lead to delays in production, shortages of critical components or materials, and increased costs for inventory management, transportation, and logistics.

Segmentation Analysis

The global market is segmented based on industry type, product type, and geography.

By Industry Type

Based on industry type, the industrial distribution industry is segmented into manufacturing, construction, oil & gas, chemicals, healthcare, and food & beverage. In 2023, the construction segment generated a revenue of USD 2,144.38 billion. This dominance can be accredited to the diverse range of products and materials required for construction projects, encompassing building materials, equipment, tools, and machinery.

With ongoing urbanization, infrastructure development, and construction projects across the globe, the demand for industrial distribution services within the construction sector continues to rise, solidifying its position as the leading segment in the market.

By Product Type

Based on product type, the industrial distribution market is classified into machinery & equipment, electrical & electronics, industrial supplies, raw materials, safety products, and others. The safety products segment is primed to record substantial growth, achieving a notable CAGR of 8.18% over the forecast period. This growth is likely to be driven by stringent regulations regarding workplace safety across various industries. Safety products, including personal protective equipment (PPE), safety apparel, signage, and emergency response equipment, are essential components of occupational health and safety protocols.

- As companies prioritize employee welfare and compliance with safety standards, the demand for safety products is expected to surge in the near future.

Industrial Distribution Market Regional Analysis

Based on region, the global market is classified into North America, Europe, Asia Pacific, MEA, and Latin America.

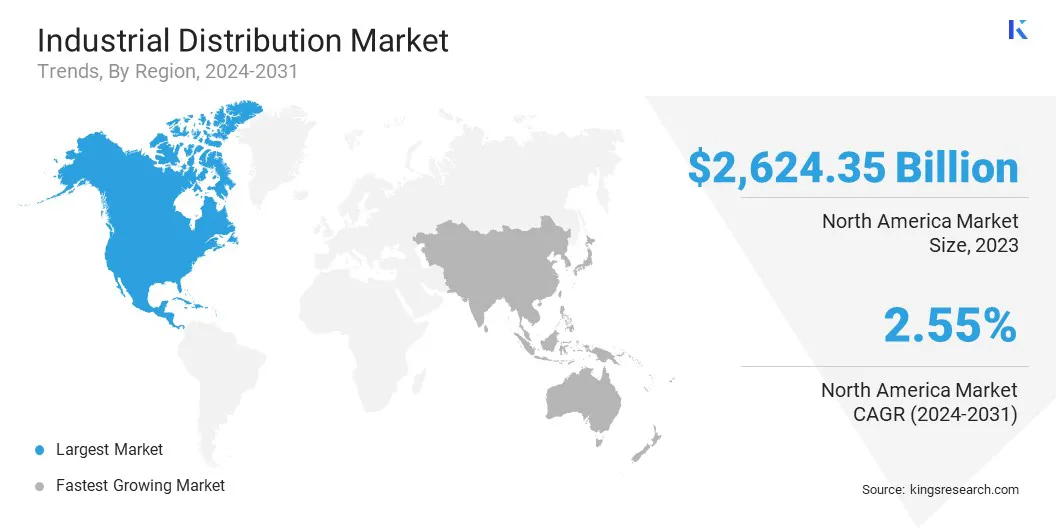

The North America Industrial Distribution Market share stood around 32.15% in 2023 in the global market, with a valuation of USD 2624.35 billion. This dominance can be attributed to the region's robust industrial base, advanced infrastructure, and strong emphasis on innovation and technology adoption. As key industries drive economic growth, the region offers a lucrative growth opportunity for industrial distributors. Additionally, several factors such as favorable business environments, strategic geographical location, and well-established trade networks contribute to its leading position in the market.

Asia Pacific is poised to experience steady progress in the industrial distribution market between 2024 and 2031, recording a significant CAGR of 8.31%. This growth is largely fueled by rapid industrialization, urbanization, and infrastructure development across countries such as China, India, and Southeast Asian nations. Rising investments in manufacturing, construction, and healthcare sectors, coupled with increasing adoption of advanced technologies, drive the demand for industrial distribution services in the region.

Similarly, the Middle East and Africa region is positioned to witness considerable growth through the assessment period, driven by infrastructure projects, oil and gas investments, and diversification efforts in non-oil sectors, which is bolstering the demand for industrial distribution solutions.

Competitive Landscape

The industrial distribution market report will provide valuable insight with an emphasis on the fragmented nature of the industry. Prominent players are focusing on several key business strategies such as partnerships, mergers and acquisitions, product innovations, and joint ventures to expand their product portfolio and increase their market shares across different regions. Expansion & investments involve a range of strategic initiatives, including investments in R&D activities, the establishment of new manufacturing facilities, and supply chain optimization, which could pose new opportunities for industrial distribution market growth.

List of Key Companies in Industrial Distribution Market

- Grainger

- MSC Industrial Direct Co., Inc.

- Fastenal Company

- Wurth Group

- Ferguson plc

- WESCO International, Inc.

- Rexel

- HD Supply Holdings, Inc.

- Sonepar

- Wolseley plc

Key Industry Developments

- July 2023 (Cooperation): India and Japan signed a Memorandum of Cooperation (MoC) to enhance collaboration in the semiconductor supply chain. This partnership aimed to strengthen the semiconductor ecosystem of both nations, facilitating technology transfer, skill development, and mutual investment opportunities. With semiconductor components being integral to various industries, including industrial distribution, this initiative signaled a strategic move to bolster India and Japan’s position in the global supply chain and promote technological advancements.

- June 2023 (Partnership): Turtle, a renowned industrial distributor, announced a renewable energy partnership with Catalyze, aimed to foster sustainability and efficiency in industrial operations. This initiative aligned with market trends toward sustainability and energy transition, offering potential cost savings and environmental benefits. By leveraging renewable energy solutions, Turtle sought to enhance their competitiveness and meet evolving customer demands for environmentally responsible practices.

The Global Industrial Distribution Market is Segmented as:

By Industry Type

- Manufacturing

- Construction

- Oil & Gas

- Chemicals

- Healthcare

- Food & Beverage

By Product Type

- Machinery & Equipment

- Electrical & Electronics

- Industrial Supplies

- Raw Materials

- Safety Products

- Others

By Region

- North America

- Europe

- France

- U.K.

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America.