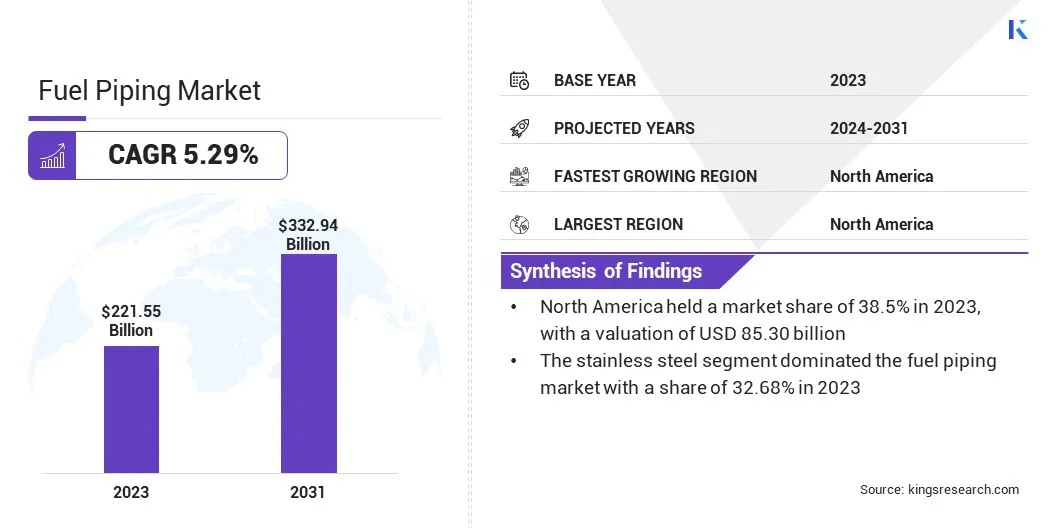

Fuel Piping Market Size

The global Fuel Piping Market size was valued at USD 221.55 billion in 2023 and is projected to reach USD 332.94 billion by 2031, growing at a CAGR of 5.29% from 2024 to 2031. In the scope of work, the report includes solutions offered by companies such as Bechtel Corporation, Tenaris S. A, Metalurgica Gerdau S. A, Valourec S. A, JFE Holdings Inc., Aliaxis Group S. A, Mexichem Sab de C.V, China Steel Corporation, Arcelor Mittal S. A, JSW Steel Limited and Others.

The global market is a vital component of the energy infrastructure, facilitating the transportation of various fuels from production facilities to distribution points. In the current market scenario, the surging demand for energy, driven by rapid industrialization and population growth, is a primary driver. The market outlook indicates sustained growth, propelled by technological advancements in piping materials and construction methods.

Innovations in corrosion-resistant coatings and eco-friendly solutions contribute to the market's efficiency and sustainability. Exploration and production activities in the oil and gas sector, along with infrastructure development, further stimulate the demand for fuel piping systems. While the transition to renewable energy is ongoing, traditional fuels still dominate, maintaining the significance of fuel piping networks.

Analyst’s Review

Key growth trends in the global market include continuous technological advancements, especially in terms of materials and construction methodologies. Innovations such as advanced materials and corrosion-resistant coatings enhance the efficiency and durability of fuel piping systems. Stringent environmental regulations are driving a shift towards eco-friendly solutions and leak detection technologies.

The escalating demand for energy, fueled by industrialization and urbanization, is a significant trend influencing fuel piping market growth. The geopolitical landscape and global events also play a crucial role in shaping the dynamics of the market.

Infrastructure development projects, particularly in emerging economies, contribute to the expansion of fuel piping networks. As the market evolves, the focus on sustainability and the exploration of renewable energy sources are likely to influence future growth trends.

Market Definition

Fuel piping is a critical component of the energy infrastructure and encompasses the network of pipelines designed for the transportation of various fuels. These pipelines serve as conduits for the movement of liquid and gaseous fuels, including petroleum products, natural gas, and aviation fuels. The primary objective of fuel piping is to establish a reliable and efficient supply chain, ensuring the seamless flow of energy resources from production and storage facilities to distribution points before it reaches end-users.

In the realm of liquid fuels, such as gasoline and diesel, fuel piping systems connect refineries and storage tanks to gas stations and industrial facilities. These pipelines play a pivotal role in meeting the demands of the transportation sector, facilitating the movement of vehicles ranging from cars to trucks.

Additionally, in the aviation industry, specialized fuel piping networks transport aviation fuels from storage facilities to airports, supporting the constant refueling of aircraft. The significance of fuel piping extends beyond land-based transportation, encompassing maritime activities as well.

Fuel piping is integral to maritime transportation, supplying vessels with the necessary fuels for their journeys, ensuring the smooth operation of shipping and naval fleets. Overall, fuel piping plays a foundational role in sustaining the global energy landscape, providing the essential infrastructure for the transportation and utilization of conventional fuels in various sectors.

Fuel Piping Market Dynamics

Escalating demand for fuel-powered transportation systems is a key driver fueling the growth of the fuel piping market. The imperative to meet the growing need for energy in the transportation sector propels the demand for efficient fuel piping networks. With urbanization and industrialization on the rise, there is a high reliance on fuel-powered vehicles for both personal and commercial transportation.

This increased demand necessitates robust fuel piping systems to ensure a steady and reliable supply of fuel to meet the mobility requirements of the global population. As the automotive and transportation industries continue to expand, the market is poised to observe steady growth, with a focus on optimizing the transportation of various fuels from source to end-user.

The fluctuating price of raw materials is a significant restraint hampering fuel piping market development. As the market heavily relies on materials such as steel, fluctuations in raw material prices can impact the overall cost of manufacturing and installation of fuel piping systems. Volatility in material costs can lead to uncertainties in project budgets and affect profit margins for companies in the market.

This challenge is particularly pronounced when dealing with materials like steel, which is commonly used in fuel piping construction. To mitigate this restraint, companies often implement strategic sourcing and risk management strategies to navigate the impact of raw material price fluctuations and maintain stability in their operations.

Segmentation Analysis

The global market is segmented based on material, end-use, and geography.

By Material

Based on material, the market is bifurcated into stainless steel, PVC, HDPE, and others. The stainless steel segment dominated the fuel piping market with a share of 32.68% in 2023 owing to its exceptional properties that make it an ideal material for fuel piping systems. Stainless steel is preferred for its corrosion resistance, durability, and ability to withstand extreme temperatures, which makes it suitable for transporting various fuels.

Additionally, stainless steel's low maintenance requirements and longevity contribute to its widespread adoption in fuel piping applications. The material's dominance is further accentuated by its compatibility with stringent industry standards and regulations, ensuring the integrity and safety of fuel transportation systems.

By End-Use

Based on end-use, the market is bifurcated into onshore and offshore. The offshore segment is expected to witness the fastest-growth, depicting a CAGR of 5.70% over the forecast period owing to the increasing focus on offshore oil and gas exploration and production activities. Offshore reserves offer significant untapped potential, and the development of these resources requires extensive fuel piping infrastructure.

The demand for offshore fuel piping is driven by the expansion of exploration activities in deep-sea locations. Additionally, advancements in offshore drilling technologies and the discovery of new reserves contribute to the accelerated growth of the offshore segment in the fuel piping market. The offshore region presents both challenges and opportunities, making it a key focal point for industry players seeking to capitalize on emerging prospects.

Fuel Piping Market Regional Analysis

Based on region, the global market is classified into North America, Europe, Asia Pacific, MEA, and Latin America.

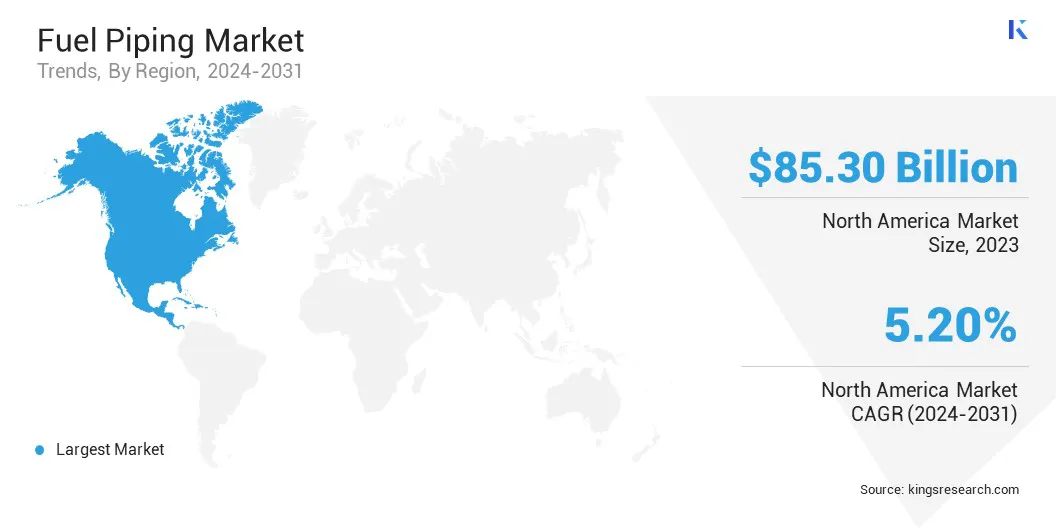

The North America Fuel Piping Market share stood around 38.5% in 2023 in the global market, with a valuation of USD 85.30 billion. The dominance of North America in the global market is attributed to well-established infrastructure, significant investments in the oil and gas sector, and a mature energy market.

The region's extensive network of pipelines for the transportation of various fuels, coupled with ongoing exploration and production activities, contributes to its leading position.

- Moreover, stringent environmental regulations drive the adoption of advanced fuel piping technologies, positioning North America at the forefront of market growth. The presence of key market players and a robust regulatory framework further solidify North America's status as a dominant force in the market.

Competitive Landscape

The fuel piping market report will provide valuable insight with an emphasis on the fragmented nature of the sector. Prominent players are focusing on several key business strategies such as partnerships, mergers & acquisitions, Source innovations, and joint ventures to expand their Source portfolios and increase their market shares across different regions.

Expansion & investments involve a range of strategic initiatives including investments in R&D activities, new manufacturing facilities, and supply chain optimization could pose new opportunities for the market.

List of Key Companies in Fuel Piping Market

- Bechtel Corporation

- Tenaris S. A

- Metalurgica Gerdau S. A

- Valourec S. A

- JFE Holdings Inc.

- Aliaxis Group S. A

- Mexichem Sab de C.V

- China Steel Corporation

- Arcelor Mittal S. A

- American Cast Iron Pipe Company

- JSW Steel Limited

Key Industry Development

- November 2023 (Partnership): NextEra Energy Partners, LP finalized a binding agreement with Kinder Morgan to divest its Texas natural gas pipeline portfolio for a total consideration of USD 1.815 billion.

The global Fuel Piping Market is segmented as:

By Material

- Stainless Steel

- PVC

- HDPE

- Others

By End-Use

By Region

- North America

- Europe

- France

- UK

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America