Energy Management Systems Market Overview

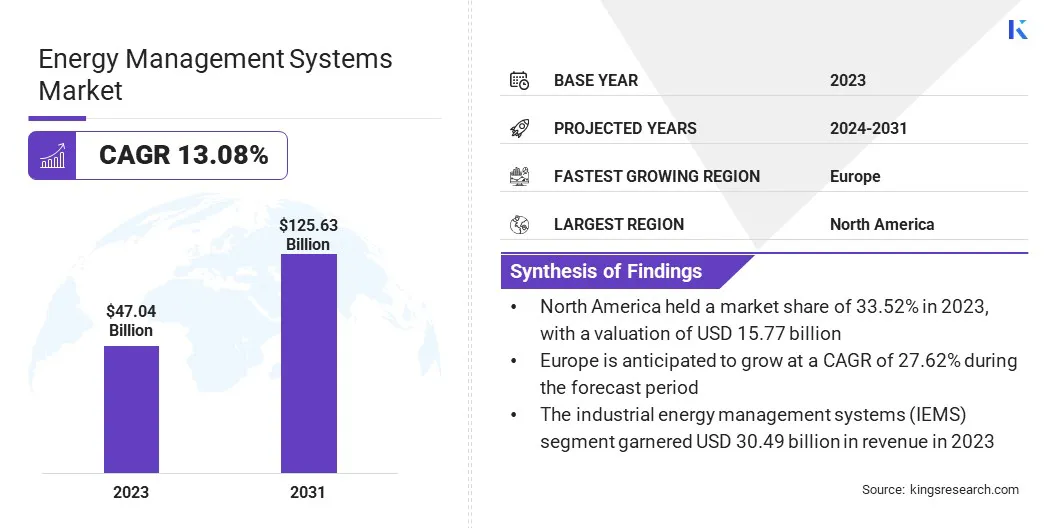

Global Energy Management Systems Market size was recorded at USD 47.04 billion in 2023, which is estimated to be at USD 53.13 billion in 2024 and projected to reach USD 125.63 billion by 2031, growing at a CAGR of 13.08% from 2024 to 2031.

The global energy management systems market is poised to witness robust growth over the forecast period, mainly driven by increasing environmental consciousness and stringent regulations concerning energy efficiency across industries worldwide.

Key Market Highlights:

- Market Value (2023): USD 47.04 Billion.

- Forecasted Value (2031): USD 125.63 Billion.

- CAGR (2024 - 2031): 13.08%.

- Largest & Fastest Growing Region (2024-2031): North America market share stood around 33.52% in 2023 in the global market, with a valuation of USD 15.77 billion.

- The residential segment is anticipated to witness the highest growth, recording a robust CAGR of 16.42% between 2024 and 2031.

- The hardware segment captured the largest market share of 65.93% in 2023.

- The industrial energy management systems (IEMS) segment garnered the highest revenue of USD 30.49 billion in 2023.

In the scope of work, the report includes solutions offered by companies such as Siemens, Schneider Electric, Eaton, Honeywell International Inc., Johnson Controls, Yokogawa Corporation, Rockwell Automation, GE Vernova, ABB, ENGIE, and others.

The growing adoption of renewable energy sources and the pressing need to optimize energy consumption are key factors propelling market expansion. Technological advancements, such as the integration of IoT, AI, and cloud computing into energy management systems, present significant growth opportunities.

Additionally, the rising demand for smart grid infrastructure and the proliferation of smart devices contribute to market growth. Emerging economies, particularly in Asia-Pacific and Middle East & Africa, offer lucrative growth opportunities due to rapid industrialization and urbanization, coupled with favorable government initiatives to promote sustainable energy practices.

Furthermore, the expansion of the industrial sector and the implementation of energy management systems in commercial buildings and residential complexes are expected to boost market growth in the coming years.

The global energy management systems market encompasses a range of technologies, software, and services designed to monitor, control, and optimize energy consumption across various sectors, including industrial, commercial, and residential.

These systems enable organizations to efficiently manage energy resources, reduce utility costs, and minimize environmental impact through advanced monitoring, analytics, and automation.

Key components of energy management systems include energy monitoring devices, software platforms for data analysis and reporting, and implementation services for system integration and optimization. The market addresses the growing demand for sustainable energy solutions, characterized by regulatory mandates, cost-saving initiatives, and increasing awareness of environmental sustainability.

Analyst’s Review

The development of the global energy management systems market is propelled by several factors such as increasing regulatory mandates for energy efficiency, rising adoption of renewable energy sources, and growing awareness of sustainability.

Moreover as companies strive to reduce their carbon footprint and operating costs, the demand for energy management systems is expected to continue to grow.

Additionally, investments in research and development for advanced technologies, including IoT, artificial intelligence, and cloud computing, are fostering competitive advantage and enabling market differentiation among key industry players.

Energy Management Systems Market Growth Factors

The integration of energy management systems (EMS) with renewable energy sources, such as solar and wind power, is revolutionizing the global energy landscape. EMS facilitates the seamless integration and effective management of distributed energy resources, thereby enhancing grid stability and resilience while promoting sustainability.

For instance, advanced EMS platforms leverage real-time data analytics to optimize the utilization of renewable energy, mitigating intermittency issues and maximizing energy efficiency. This integration is reducing reliance on fossil fuels and enabling businesses and utilities to capitalize on renewable energy incentives and regulatory frameworks, thereby bolstering both economic and environmental benefits.

Furthermore, the escalating costs of traditional energy sources and the implementation of carbon pricing mechanisms are compelling organizations to prioritize energy efficiency and carbon reduction strategies. Energy management systems offer a comprehensive solution, enabling companies to monitor, analyze, and optimize energy usage, thereby minimizing operational costs and carbon emissions.

For instance, industries subject to carbon pricing schemes are leveraging EMS to identify energy-intensive processes and implement targeted efficiency measures, leading to a reduction of their carbon tax liabilities.

Moreover, EMS empowers businesses to proactively manage energy consumption patterns, aligning with sustainability goals and enhancing corporate social responsibility initiatives. However, the high initial investment costs associated with EMS solutions pose a challenge for businesses, particularly SMEs, thus highlighting the need for innovative financing models to improve accessibility.

Additionally, limited awareness regarding EMS benefits, especially in smaller businesses, and the lack of standardized protocols across the industry, are hindering the widespread adoption. EMS providers are striving to provide strategic pricing and subscription-based models to overcome these challenges.

Energy Management Systems Market Trends

The convergence of information technology (IT) and operational technology (OT) within EMS is signifying a paradigm shift in energy management practices. This integration enables real-time data analysis and automation, empowering organizations to make informed decisions swiftly and optimize energy management processes efficiently.

Additionally, the proliferation of smart meters, sensors, and connected devices has led to an exponential increase in data volume, thus boosting the adoption of big data analytics in EMS. By leveraging big data analytics, organizations are identifying energy usage patterns, pinpointing inefficiencies, and creating opportunities for further optimization, thereby enhancing overall energy efficiency.

Furthermore, the integration of artificial intelligence (AI) and machine learning is augmenting EMS capabilities by enabling predictive analytics and automated optimization strategies. These advanced technologies facilitate anomaly detection and proactive energy management, empowering organizations to achieve greater efficiency, sustainability, and cost savings in their energy operations.

Segmentation Analysis

The global energy management systems market is segmented based on type, component, deployment, end user, and geography.

By Type

Based on type, the market is categorized into industrial energy management systems (IEMS), building energy management systems (BEMS), and home energy management systems (HEMS). The industrial energy management systems (IEMS) segment garnered the highest revenue of USD 30.49 billion in 2023.

Industries exhibit high energy consumption levels due to their manufacturing processes and operational activities. Furthermore, the demand for refined energy management solutions to optimize energy usage and reduce costs is increasing.

Additionally, stringent regulatory requirements compel industrial facilities to invest in advanced IEMS to ensure compliance with energy efficiency standards and mitigate environmental impact. Furthermore, the increasing adoption of automation and digitalization in industrial settings propels the implementation of IEMS for the real-time monitoring, analysis, and optimization of energy-intensive processes.

By Component

Based on component, the market is divided into hardware, software, and services. The hardware segment captured the largest market share of 65.93% in 2023. Hardware components such as sensors, meters, and control devices form the fundamental infrastructure of EMS, facilitating data collection, monitoring, and control of energy consumption.

The increasing deployment of smart meters and IoT-enabled sensors in various industries and buildings is leading to an increased demand for hardware components, enabling real-time data acquisition and analysis for informed decision-making.

Moreover, advancements in hardware technology, including the development of energy-efficient devices and robust communication protocols, enhance the functionality and reliability of EMS hardware solutions.

By End User

Based on end user, the market is categorized into residential, energy & power, telecom & it, manufacturing, commercial, food & beverage, and others. The residential segment is anticipated to witness the highest growth, recording a robust CAGR of 16.42% between 2024 and 2031.

Increasing consumer awareness regarding energy efficiency and sustainability is fostering the adoption of residential energy management systems. With rising energy costs and mounting environmental concerns, homeowners are seeking solutions to optimize energy usage and reduce utility expenses, thereby fueling demand for residential EMS.

Moreover, advancements in technology, such as smart home automation and IoT integration, make it easier for homeowners to monitor and control energy consumption remotely, resulting in widespread adoption. Additionally, government incentives and rebate programs aimed at promoting energy-efficient practices incentivize homeowners to invest in EMS solutions.

Energy Management Systems Market Regional Analysis

Based on region, the global energy management systems market is classified into North America, Europe, Asia-Pacific, MEA, and Latin America.

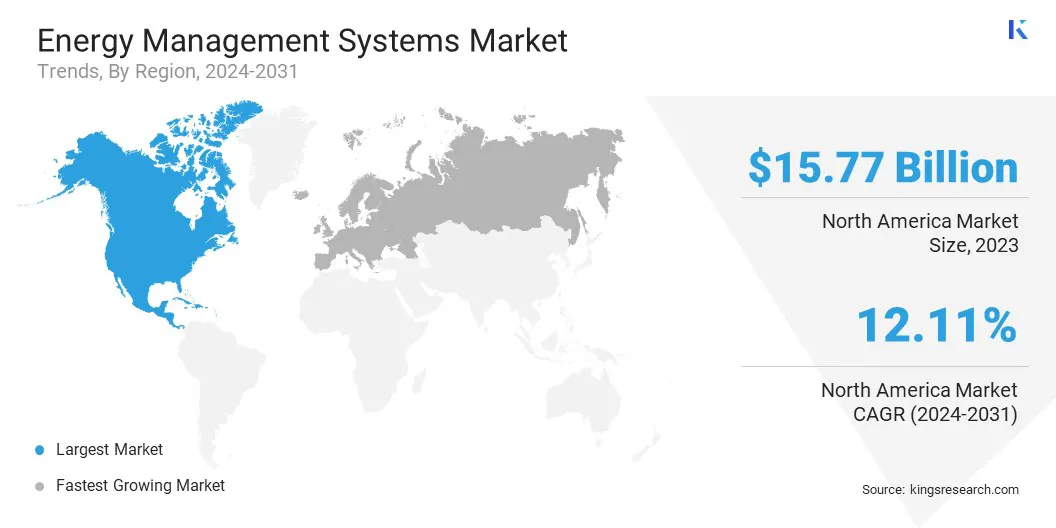

The North America Energy Management Systems Market share stood around 33.52% in 2023 in the global market, with a valuation of USD 15.77 billion. This notable growth is mainly attributed to stringent energy efficiency regulations imposed at federal and state levels in response to rising concerns over climate change and energy security. These factors are propelling the demand for advanced EMS solutions across diverse industries.

Moreover, the region's growing emphasis on smart city initiatives and grid modernization projects underscores the surging need for integrated energy management systems to optimize resource allocation and enhance grid resilience.

The concentration of large manufacturing facilities and commercial buildings in North America presents a conducive environment for EMS investments. Furthermore, the expansion of demand response programs, coupled with the increasing participation from commercial and industrial facilities, is presenting opportunities for EMS providers.

Europe accounted for a significant share of 27.62% in 2023. The ambitious targets set by the EU for energy efficiency and greenhouse gas reduction are resulting in the increased adoption of EMS solutions across various sectors.

Stricter energy performance standards for buildings and industries necessitate advanced EMS implementations to meet compliance requirements while optimizing energy usage. Furthermore, the high energy prices observed in Europe compared to other global regions incentivize businesses to invest in EMS for cost savings and enhanced energy security.

Moreover, Europe's focus on developing regional energy trading platforms and microgrids is offering opportunities for EMS providers to facilitate efficient energy exchange within diverse markets. Retrofitting aging buildings with intelligent EMS solutions addresses the region's emphasis on energy efficiency, while the integration of EMS with electric vehicle charging infrastructure aligns with the growing EV market's energy management needs.

Competitive Landscape

The global energy management systems market report will provide valuable insight with an emphasis on the fragmented nature of the industry. Prominent players are focusing on several key business strategies such as partnerships, mergers and acquisitions, product innovations, and joint ventures to expand their product portfolio and increase their market shares across different regions.

Companies are implementing impactful strategic initiatives, such as expanding services, investing in research and development (R&D), establishing new service delivery centers, and optimizing their service delivery processes, which are likely to create new opportunities for market growth.

Key Companies in Energy Management Systems Market

- Siemens

- Schneider Electric

- Eaton

- Honeywell International Inc.

- Johnson Controls

- Yokogawa Corporation

- Rockwell Automation

- GE Vernova

- ABB

- ENGIE

Key Industry Developments

- August 2023 (Acquisition): Tango, a prominent supplier of cloud-based software for real estate and facilities management, acquired WatchWire. WatchWire, known for its expertise in data and analytics, assists companies in lowering emissions and energy costs while streamlining sustainability and carbon reporting processes. The acquisition of WatchWire by Tango will enhance their capabilities in providing comprehensive solutions for sustainable real estate management.

The Global Energy Management Systems Market is Segmented as:

By Type

- Industrial Energy Management Systems (IEMS)

- Building Energy Management Systems (BEMS)

- Home Energy Management Systems (HEMS)

By Component

- Hardware

- Software

- Services

By Deployment

By End User

- Residential

- Energy & Power

- Telecom & IT

- Manufacturing

- Commercial

- Food & Beverage

- Others

By Region

- North America

- Europe

- France

- U.K.

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America