eHealth Market Size

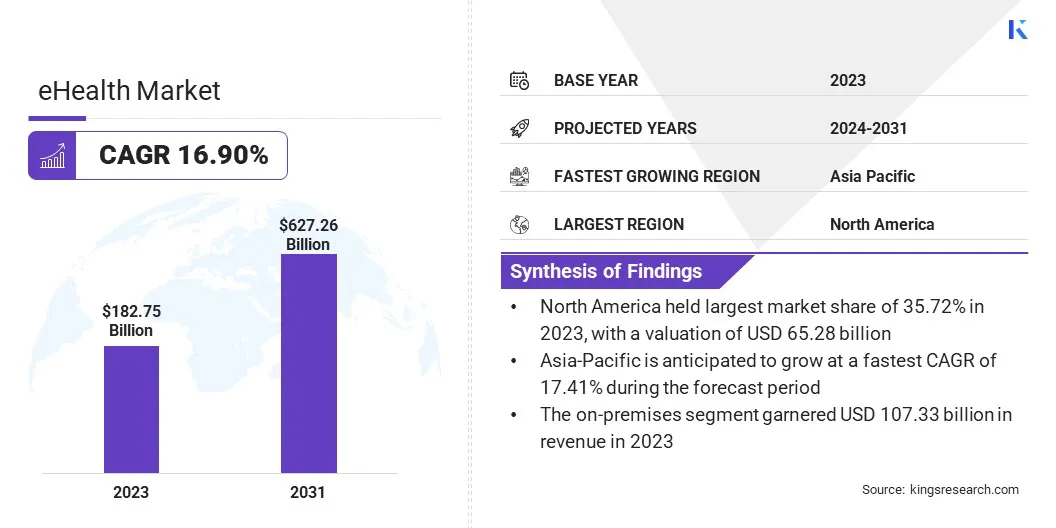

The Global eHealth Market size was valued at USD 182.75 billion in 2023 and is projected to grow from USD 210.24 million in 2024 to USD 627.26 billion by 2031, exhibiting a CAGR of 16.90% over the forecast period.

The aging population and increasing prevalence of chronic diseases are driving the growth of the market, increasing the demand for remote health monitoring, personalized care, and continuous disease management to improve outcomes for long-term health conditions through digital solutions.

In the scope of work, the report includes services offered by companies such as Oracle, Epic Systems Corporation, MCKESSON CORPORATION, American Well Corporation., Veradigm LLC, athenahealth, Inc, Philips International B.V, UnitedHealth Group, Medtronic, GE HealthCare, and others.

The eHealth market is revolutionizing healthcare by integrating digital technologies into traditional systems, enhancing accessibility, efficiency, and patient care. It enables seamless communication and data exchange between patients and providers, fostering a more connected healthcare ecosystem.

Digital tools such as telemedicine, mobile health apps, and wearable devices empower patients to manage their health remotely, while healthcare professionals benefit from streamlined operations and more accurate diagnoses. By improving patient engagement, enabling personalized care, and reducing inefficiencies, eHealth is transforming healthcare delivery. As technology advances, the market is integral to shaping more accessible and efficient healthcare systems.

- In November 2024, Teladoc Health introduced AI-enhanced features in its Virtual Sitter solution to improve patient safety, address workforce challenges, and reduce hospital falls. This innovation supports market expansion by enhancing healthcare accessibility, efficiency, and patient care.

The market involves the use of digital technologies and electronic communication tools to enhance healthcare delivery, improve patient outcomes, and streamline healthcare processes. It encompasses a broad range of technologies, such as telemedicine, electronic medical records, wearable devices, and electronic health records, which enable healthcare providers to offer more efficient, accessible, and personalized care.

By integrating digital solutions into traditional healthcare systems, the eHealth market supports real-time data exchange, remote monitoring, and virtual consultations, making healthcare more convenient and accessible, particularly in underserved or remote areas. It aims to improve overall healthcare efficiency, reduce costs, enhance patient engagement.

- In December 2024, Epic Nexus, a Trusted Exchange Framework and the Common Agreement (TEFCA) Qualified Health Information Network, connected 625 hospitals, advancing secure medical records exchange nationwide. TEFCA, established under the 21st Century Cures Act, is part of Epic's ongoing commitment to interoperability. Currently, all U.S. health systems using Epic are interoperable, improving care coordination and clinical outcomes by making patient data readily accessible.

Analyst’s Review

Analyst’s Review

The eHealth market is transforming healthcare by reducing costs, enhancing efficiency, and empowering patients. Digital technologies such as virtual consultations, AI diagnostics, and wearable devices streamline healthcare processes, reduce operational costs, and optimize resources.

By promoting preventive care, early intervention, and self-management, eHealth solutions lower the need for expensive treatments and hospital visits. This shift toward digital healthcare is fostering a more efficient, patient-centered approach, improving clinical outcomes and delivering long-term savings for healthcare systems.

- In December 2024, All India Institute of Medical Sciences (AIIMS), New Delhi, partnered with Wipro GE Healthcare to establish an AI Health Innovations Hub. The hub focuses on developing AI-driven solutions for precise diagnosis and real-time patient data tracking. Wipro GE Healthcare is investing $1 million over five years, with AIIMS providing clinical inputs and real-world evaluation.

eHealth Market Growth Factors

The rising focus on preventive care has emerged as a key factor propelling the growth of the eHealth market. Through AI-powered platforms and personalized health insights, individuals can actively monitor their health and detect potential issues early.

Tele-eHealth consultations enhance this approach by offering timely guidance and interventions. This proactive model reduces the risk of serious health conditions and helps avoid costly treatments, hospitalizations, and emergency care. By promoting early detection and ongoing health management, preventive care solutions improve overall health outcomes and lower long-term healthcare costs, fueling market expansion.

- In September 2023, Paige partnered with Microsoft to advance cancer diagnosis and patient care by developing the world’s largest image-based AI models for digital pathology and oncology. By using over one billion images from half a million pathology slides, they are creating an AI model with billions of parameters to enhance cancer detection and enable next-generation clinical applications.

Data security presents a significant challenge to the expansion of the eHealth market, as the increasing amount of sensitive patient data exchanged increases vulnerability to cyberattacks and breaches.

To address this challenge, robust cybersecurity measures, including encryption, multi-factor authentication, and advanced threat detection systems, are essential to protect patient privacy. Regular security audits and compliance with data protection regulations, can further strengthen trust in eHealth solutions, ensuring their continued adoption and safeguarding against security risks.

eHealth Industry Trends

A significant trend in the eHealth market is the growing adoption of wearables and remote health monitoring devices. These technologies allow real-time tracking of vital signs, shifting healthcare management from reactive to proactive.

By continuously monitoring metrics such as heart rate, blood pressure, and glucose levels, they enable early detection of potential health issues, leading to improved patient outcomes. This trend is enhancing both individual health management and the efficiency of healthcare delivery.

- In September 2024, Apple unveiled new sleep and hearing health features for Apple Watch, enhancing users' health management. The Breathing Disturbances metric, which includes sleep apnea notifications, is pending FDA approval. These features will be available in over 150 countries, including the U.S., EU, and Japan.

Another key trend in the eHealth market is the advancement of interoperability, which improves data sharing and integration across healthcare systems. This allows for seamless access to patient information, enhancing care coordination.

Better integration allows healthcare providers to access up-to-date patient data, leading to informed decisions, fewer errors, and improved outcomes. These advancements are crucial for creating a connected healthcare ecosystem, ensuring timely and efficient care across various settings or providers.

- In March 2024, Carequality, a nationwide interoperability trust framework, marked its 10th anniversary. It facilitates the exchange of over 745 million documents monthly across diverse technologies, geographies, and networks. Carequality has played a key role in enabling seamless health information exchange between health information networks, enhancing care coordination, and improving patient outcomes.

Segmentation Analysis

The global market has been segmented based on type, deployment, service and end user, and geography.

By Type

Based on type, the market has been segmented into health information systems, e-Prescribing, clinical decision support systems, telemedicine, and others. The health information systems segment led the eHealth market in 2023, reaching a valuation of USD 46.71 billion. The expansion of health information systems in the market is rapidly transforming healthcare by enabling more efficient, data-driven care.

Health information systems, including electronic health records, electronic medical record, patient engagement solution and population health management, are increasingly adopted to streamline healthcare operations, enhance care coordination, and improve patient outcomes.

As healthcare organizations move towards digital solutions, the integration of cloud computing, AI, and big data analytics further accelerates health information systems capabilities, allowing for real-time data sharing, predictive analytics, and personalized treatments. This growth fosters a more patient-centric, cost-effective, and accessible healthcare environment, driving the global market forward.

By Deployment

Based on deployment, the eHealth market has been bifurcated into on-premises and cloud-based. The on-premises segment secured the largest revenue share of 58.73%.

On-premises deployment refers to the integration of digital health technologies within healthcare facilities, such as hospitals or clinics, to streamline operations and enhance patient care. This includes installing systems such as electronic health records systems, telemedicine platforms, and diagnostic tools on-site, providing greater control over data security, compliance, and customization.

By managing technology in-house, healthcare providers can ensure faster data access, improve care coordination, and reduce dependence on external cloud services. On-premises deployment supports more efficient workflows, secure patient data management, and better integration across various healthcare departments.

By Service

Based on service, the market has been classified into remote monitoring, diagnosis & consultation, database management, treatment, and healthcare systems strengthening. The diagnosis & consultation segment is poised to witness significant growth at a staggering CAGR of 16.06%.

eHealth is widely used in diagnostics and healthcare due to its ability to enhance accuracy, efficiency, and accessibility. Digital health tools enable healthcare professionals to make faster, more informed decisions. These technologies provide real-time access to patient data, allowing for improved diagnosis, personalized treatment plans, and more effective disease management.

Additionally, remote monitoring tools and mobile health apps empower patients to actively engage in their health journey, promoting early detection and reducing hospital visits. The integration of eHealth solutions helps streamline processes, reduce costs, and improve overall healthcare quality.

eHealth Market Regional Analysis

Based on region, the global market has been classified into North America, Europe, Asia-Pacific, MEA, and Latin America.

The North America eHealth market accounted for a substantial share of around 35.72% in 2023, with a valuation of USD 65.28 billion. This growth is primarily fueled by advanced healthcare infrastructure, widespread adoption of digital technologies, and strong government support for health IT initiatives.

The North America eHealth market accounted for a substantial share of around 35.72% in 2023, with a valuation of USD 65.28 billion. This growth is primarily fueled by advanced healthcare infrastructure, widespread adoption of digital technologies, and strong government support for health IT initiatives.

Furthermore, the regional market benefits from the presence of leading healthcare providers and technology companies, fostering the integration of electronic health records, telemedicine, and AI-based solutions. A robust regulatory framework ensures data security and patient privacy, building trust in eHealth. The growing demand for efficient, accessible, and personalized healthcare, combined with high healthcare spending, further bolsters domestic market expansion.

The Asia-Pacific eHealth market is set to witness notable growth over the forecast period, registering a robust CAGR of 17.41%. This expansion is mainly fueled by rapid technological advancements, increasing healthcare demands, and a growing population. The region's diverse population highlights the need for affordable and accessible healthcare solutions, boosting the adoption of digital health technologies such as telemedicine, wearable devices, and mobile health apps.

Government initiatives supporting digital healthcare infrastructure, along with rising awareness of preventive care, further fuel domestic market growth. Additionally, expanding internet and smartphone penetration increases the demand for eHealth tools. As healthcare systems modernize and adopt digital transformation, the Asia Pacific market is experiencing significant expansion.

- The National Digital Health Mission (NDHM), in line with the National Health Policy (NHP) 2017 and the National Digital Health Blueprint aims to create a robust digital infrastructure for secure and standardized healthcare delivery in while ensuring data confidentiality and advancing universal health coverage.

Competitive Landscape

The global eHealth market report will provide valuable insight with an emphasis on the fragmented nature of the industry. Prominent players are focusing on several key business strategies such as partnerships, mergers and acquisitions, product innovations, and joint ventures to expand their product portfolio and increase their market shares across different regions.

Strategic initiatives, including investments in R&D activities, the establishment of new manufacturing facilities, and supply chain optimization, could create new opportunities for market growth.

List of Key Companies in eHealth Market

- Oracle

- Epic Systems Corporation

- MCKESSON CORPORATION

- American Well Corporation.

- Veradigm LLC

- athenahealth, Inc

- Philips International B.V

- UnitedHealth Group

- Medtronic

- GE HealthCare

Key Industry Developments

- October 2024 (Launch): Oracle introduced its next-generation electronic health record at the Oracle Health Summit. Built on Oracle Cloud Infrastructure (OCI), the EHR leverages AI to optimize clinical workflows, automate tasks, and provide real-time insights at the point of care. It stramlines appointment preparation, documentation, follow-ups, provider-payer data exchange, clinical trial recruitment, and regulatory compliance, all while enhancing financial and advancing value-based care adoption.

- January 2024 (Launch): Eli Lilly and Company introduced LillyDirect, a digital healthcare platform for U.S. patients with obesity, migraine, and diabetes. The platform provides disease management resources, access to independent healthcare providers, and home delivery of select Lilly medications through third-party pharmacies.

The global eHealth market has been segmented as:

By Type

- Health Information Systems

- Electronic Health Record

- Electronic Medical Record

- Patient Engagement Solution

- Population Health Management

- e-Prescribing

- Clinical Decision Support Systems

- Telemedicine

- Others

By Deployment

By Service

- Remote Monitoring

- Diagnosis & Consultation

- Database Management

- Treatment

- Healthcare Systems Strengthening

By End User

- Healthcare Providers

- Hospitals

- Ambulatory Care Centers

- Others

- Payers

- Healthcare Consumers

- Others

By Region

- North America

- Europe

- France

- UK

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America