Data Center Cooling Market Size

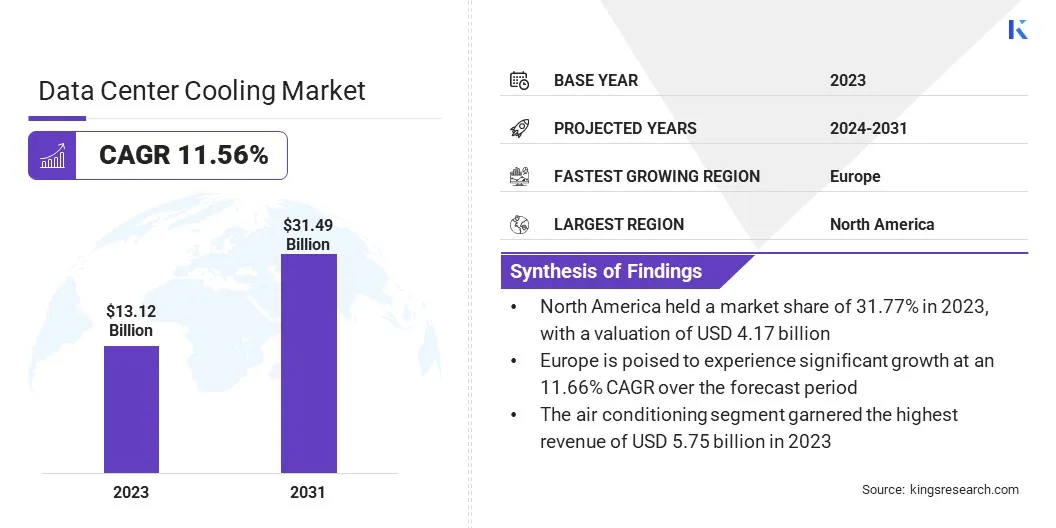

The global Data Center Cooling Market size was valued at USD 13.12 billion in 2023 and is projected to reach USD 31.49 billion by 2031, growing at a CAGR of 11.56% from 2024 to 2031. In the scope of work, the report includes solutions offered by companies such as Rittal GmbH & Co. KG, Vertiv Group Corp., LiquidStack Holding B.V., Schneider Electric, Johnson Controls, Hitachi, Ltd., Munters, Asetek Inc., DAIKIN INDUSTRIES, Ltd., FUJITSU and Others.

The development of next-generation cooling technologies is contributing significantly to market development. With the ever-increasing demand for data storage and processing capabilities, traditional cooling methods are proving insufficient in handling the heat generated by modern high-density server racks. As a result, there is a rising demand for innovative cooling solutions that are energy-efficient and capable of effectively dissipating heat in densely packed data center environments.

The data center cooling industry is experiencing the emergence of several next-generation cooling technologies such as liquid immersion cooling, direct-to-chip cooling, and advanced air-based cooling systems. These technologies leverage cutting-edge engineering and materials to enhance thermal management within data centers, resulting in higher efficiency and lower operating costs.

Data center cooling is a solution designed to regulate the temperature and humidity levels within data center facilities, thus ensuring optimal performance and reliability of IT equipment.

These solutions diverge in type, including air-based cooling systems such as precision air conditioning units and computer room air handlers (CRAHs), liquid-based cooling systems such as chilled water systems and immersion cooling, as well as hybrid approaches that combine both air and liquid cooling techniques.

The wide range of products in the data center cooling market includes cooling units, heat exchangers, cooling towers, pumps, and control systems designed to regulate temperature and airflow efficiently.

Industries with significant reliance on data center cooling solutions include IT and telecommunications, banking and finance, healthcare, government, and various other sectors with extensive data processing and storage needs. As data centers continue to expand, the demand for innovative cooling solutions tailored to specific industry requirements is expected to rise.

Analyst’s Review

Several factors such as the proliferation of cloud computing, big data analytics, and IoT applications are contributing to the growing demand for data center cooling solutions. Key players are implementing strategies to capitalize on these factors by focusing on innovative cooling technologies, energy efficiency, and sustainability.

The adoption of advanced cooling solutions, such as liquid cooling and containment systems, is on the rise, with significant investments in AI-powered management platforms for optimized cooling infrastructure. Moreover, strategic partnerships and acquisitions aimed at expanding product portfolios and extending geographic reach are key imperatives for players striving to maintain a competitive edge in the market.

Data Center Cooling Market Growth Factors

The data center cooling market is witnessing notable expansion attributed to the increasing demand for energy-efficient cooling systems. Several types of energy-efficient cooling systems include air cooling, liquid cooling, and evaporative cooling. Rising energy costs and growing environmental concerns are significant factors propelling the adoption of energy-efficient cooling systems in data centers.

Organizations are increasingly turning to energy-efficient cooling technologies such as precision cooling units, economizers, and containment solutions to minimize energy consumption and enhance sustainability. By deploying these solutions, data center operators are effectively reducing their operational expenses while demonstrating their commitment to environmental stewardship by lowering greenhouse gas emissions associated with cooling operations.

The complexity of liquid cooling systems, which requires higher installation and maintenance expenses compared to traditional air-based systems, is hampering market development. Despite the long-term benefits in terms of energy savings and operational efficiency, the higher upfront costs associated with liquid cooling systems deter organizations from adopting these technologies, particularly smaller enterprises with limited capital budgets.

- Industry stakeholders are focusing on addressing several key challenges such as overcoming cost barriers and demonstrating the long-term return on investment of liquid cooling solutions to accelerate widespread adoption.

Data Center Cooling Market Trends

A notable trend in the data center cooling market is the increasing adoption of liquid cooling solutions, marking a significant shift from traditional air-based cooling methods. Liquid cooling offers several advantages over air cooling, including higher thermal efficiency, improved cooling capacity, and reduced energy consumption.

With the increasing power densities and heat loads of modern IT equipment, particularly in hyper scale and high-performance computing environments, liquid cooling has emerged as a viable solution to effectively manage heat dissipation and ensure optimal operating conditions.

Moreover, liquid cooling enables precise temperature control and eliminates the need for raised floor systems and extensive airflow management, leading to greater flexibility in data center design and layout. As a result, data center operators are increasingly exploring various liquid cooling technologies such as direct-to-chip cooling, immersion cooling, and cold plate cooling to enhance thermal management capabilities and meet the evolving demands of next-generation data centers.

Segmentation Analysis

The global market is segmented based on component, type, product, industry, and geography.

By Component

Based on component, the market is bifurcated into solutions and services. The solution segment captured the largest data center cooling market share of 75.13% in 2023, driven by the increasing demand for comprehensive cooling solutions tailored to meet the specific requirements of data center environments.

It includes a wide range of products and services such as precision cooling units, containment systems, heat exchangers, and cooling management software, specifically designed to optimize thermal performance and energy efficiency for data centers.

Additionally, advancements in cooling technologies and the emphasis on sustainable practices have spurred investments in holistic cooling solutions that encompass both hardware and software components, thereby supporting the growth of the segment.

By Product

Based on product, the data center cooling market is categorized into air conditioning, air handling & chilling units, liquid cooling systems, and others. The air conditioning segment garnered the highest revenue of USD 5.75 billion in 2023, propelled by the widespread adoption of air-based cooling systems in data center environments.

The dominance of the air conditioning segment can be attributed to several factors, including the familiarity and maturity of air-based cooling technologies, their relatively lower upfront costs compared to liquid cooling solutions, and compatibility with existing data center infrastructure.

Additionally, advancements in precision cooling technologies, such as variable speed compressors, advanced airflow management, and intelligent control systems, have improved the energy efficiency and performance of air conditioning units.

By Industry

Based on industry, the market is segmented into BFSI, IT & telecommunications, government & defense, retail, healthcare, and others. The retail segment is anticipated to witness the highest growth at a CAGR of 12.93% over the forecast period.

The growth in e-commerce activities, particularly driven by the proliferation of online shopping platforms and digital payment systems, has led to a surge in data generation and storage requirements, thereby driving demand for retail data center services.

Furthermore, the adoption of edge computing technologies to deliver low-latency services and support real-time applications is driving the deployment of distributed data centers directly to end-users, thereby fueling the growth of the segment. As retail companies seek to enhance their digital capabilities and ensure seamless customer experiences, investments in retail data center infrastructure are expected to increase, thereby stimulating the growth of the segment.

Data Center Cooling Market Regional Analysis

Based on region, the global market is classified into North America, Europe, Asia-Pacific, MEA, and Latin America.

The North America data center cooling market share stood around 31.77% in 2023 in the global market, with a valuation of USD 4.17 billion.

The robust expansion of digital infrastructure driven by the proliferation of cloud computing, big data analytics, and the Internet of Things (IoT) is contributing significantly to regional market expansion. The presence of hyper scale data centers operated by tech giants, cloud service providers, and enterprises is creating substantial demand for advanced cooling solutions to support their operations.

Additionally, stringent regulations and environmental mandates in the region regarding energy efficiency and carbon emissions have propelled investments in energy-efficient cooling technologies and sustainable data center practices. Moreover, the region's prominent position in the market is bolstered by its favorable business environment, access to advanced technologies, and strong support for innovation.

- For instance, in May 2022, Intel revealed a significant investment to advance sustainable data center technology solutions which involves USD 700 million in funding for a 200,000-square-foot research and development mega lab. It focuses on innovative data center technologies, including heating, cooling, and water usage optimization.

Europe is poised to experience significant growth at an 11.66% CAGR in the foreseeable future. This notable expansion is mainly attributed to the increasing adoption of cloud computing, digital transformation initiatives, and the widespread adoption of emerging technologies such as artificial intelligence (AI), machine learning, and edge computing across the region.

As businesses across diverse sectors increasingly prioritize digitalization and seek to utilize the power of data-driven insights, the demand for robust and efficient data center infrastructure, including advanced cooling solutions, is expected to surge.

Furthermore, the European Union's focus on sustainability and environmental stewardship, as evidenced by initiatives such as the Green Deal and stringent regulations on energy efficiency, is prompting investments in energy-efficient cooling technologies and sustainable data center practices.

Competitive Landscape

The data center cooling market report will provide valuable insight with an emphasis on the fragmented nature of the industry. Prominent players are focusing on several key business strategies such as partnerships, mergers and acquisitions, product innovations, and joint ventures to expand their product portfolio and increase their market shares across different regions.

Manufacturers are adopting a range of strategic initiatives, including investments in R&D activities, the establishment of new manufacturing facilities, and supply chain optimization, to strengthen their market standing.

List of Key Companies in Data Center Cooling Market

- Rittal GmbH & Co. KG

- Vertiv Group Corp.

- LiquidStack Holding B.V.

- Schneider Electric

- Johnson Controls

- Hitachi, Ltd.

- Munters

- Asetek Inc.

- DAIKIN INDUSTRIES, Ltd.

- FUJITSU

Key Industry Developments

- April 2024 (Launch): Carrier Global Corporation entered into a partnership with Strategic Thermal Labs to utilize STL's pioneering technology for a liquid cooling solution tailored for data centers.

- March 2024 (Launch): Schneider Electric revealed a partnership with NVIDIA aimed at enhancing data center infrastructure to facilitate breakthroughs in edge artificial intelligence (AI) and digital twin technologies. The emphasis is placed on facilitating high-power distribution, liquid-cooling systems, and user-friendly controls for reliable operations.

- March 2024 (Collaboration): Gates collaborated with CoolIT Systems for the expansion of data center cooling which aims to address the increasing demand within the AI, high-performance computing (HPC), and enterprise sectors.

- December 2023 (Acquisition): Vertiv finalized a definitive agreement to acquire all shares of CoolTera, bolstering its coolant distribution infrastructure for data center liquid cooling technology.

The global Data Center Cooling Market is Segmented as:

By Component

By Type

- Room-based

- Row/Rack-based

By Product

- Air Conditioning

- Air Handling & Chilling Units

- Liquid Cooling Systems

- Others

By Industry

- BFSI

- IT & Telecommunications

- Government & Defense

- Retail

- Healthcare

- Others

By Region

- North America

- Europe

- France

- U.K.

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America