Market Definition

Barrier films are specialized packaging materials designed to protect contents from moisture, oxygen, light, and other environmental factors that can degrade product quality. The market encompasses films made from polyethylene, polypropylene, polyethylene terephthalate, polyamides, ethylene vinyl alcohol, and specialty polymers.

These films are offered in metalized, transparent, and white variants, in single or multiple layers, and are used in pouches, bags, blister packs, and other formats across food and beverages, pharmaceuticals, agriculture, and industrial applications.

Barrier Films Market Overview

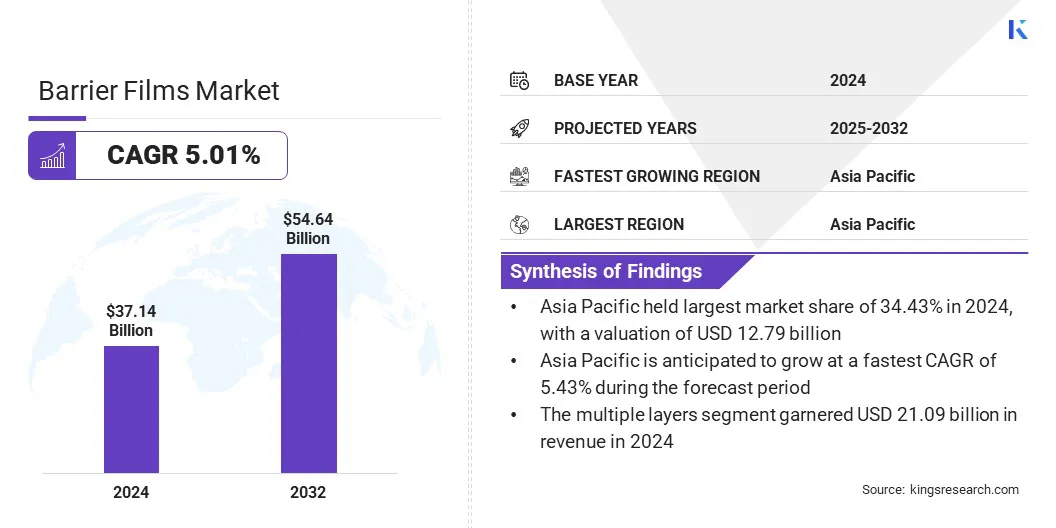

The global barrier films market size was valued at USD 37.14 billion in 2024 and is projected to grow from USD 38.80 billion in 2025 to USD 54.64 billion by 2032, exhibiting a CAGR of 5.01% during the forecast period.

This market is experiencing steady growth due to the rising demand for advanced packaging solutions that extend product shelf life and preserve quality. Expanding consumption of packaged food and beverages, along with the increasing adoption of high-performance materials in pharmaceutical packaging, is further driving market expansion.

Key Highlights

- The barrier films industry size was recorded at USD 37.14 billion in 2024.

- The market is projected to grow at a CAGR of 5.01% from 2025 to 2032.

- Asia Pacific held a market share of 34.43% in 2024, with a valuation of USD 12.79 billion.

- The polyethylene (PE) segment garnered USD 12.41 billion in revenue in 2024.

- The metalized barrier films segment is projected to attain a valuation of USD 26.99 billion by 2032.

- The multiple layer’s segment is expected to reach USD 32.23 billion by 2032.

- The pouches segment is anticipated to reach a value of USD 27.66 billion by 2032.

- The food and beverage packaging segment is predicted to generate USD 23.39 billion by 2032.

- The market in North America is anticipated to grow at a CAGR of 5.04% over the forecast period.

Major companies operating in the barrier films market are Amcor plc, Sealed Air, Mondi, Cosmo Films, TEIJIN LIMITED, TOPPAN Inc., Huhtamäki Oyj, Winpak LTD., Celplast Metallized Products, B.C. Jindal group, Glenroy, Inc., Toray Industries, Inc., Schur Hagen & Sivertsen, FLAIR Flexible Packaging Corporation, and HPM GLOBAL.

Technological advancements in polymer formulations and coating processes are enhancing protection against oxygen, moisture, and light, extending the shelf life of food, pharmaceutical, and industrial products.

Manufacturers are developing mono-material and recyclable films that combine performance with sustainability. These innovations result in flexible, durable, and cost-effective packaging solutions, supporting expanding barrier film applications across diverse industries and regions.

- In March 2025, Klöckner Pentaplast introduced high-barrier pharmaceutical films, including alfoil, Aclar, and kpNext RB5, to protect medicines from moisture, oxygen, and light while supporting sustainability.

Market Driver

Expansion of Pharmaceutical Production Boosting Packaging Demand

Growth in the barrier films market is driven by the expansion of the pharmaceutical industry. The increasing production of medicines and sensitive healthcare products requires packaging solutions that ensure stability, protect against moisture, oxygen, and light, and maintain product efficacy throughout the supply chain. The growing focus on regulatory compliance and drug safety further reinforces the need for high-performance films.

- In April 2025, Roche announced a USD 50 billion investment in the United States over five years to expand and upgrade its pharmaceutical and diagnostics R&D and manufacturing facilities.

As pharmaceutical manufacturing scales up globally, the demand for reliable, durable, and advanced barrier films rises proportionally. Pharmaceutical packaging serves as a key contributor to the overall expansion of the market, highlighting the close link between industry growth and packaging requirements.

Market Challenge

Recycling and Sustainability Challenges in Barrier Films

A major challenge in the barrier films market is ensuring environmental sustainability, as most barrier films are made of plastic polymers, and many high-performance films, particularly multi-layer and metalized variants, are difficult to recycle due to the combination of different polymers and coatings.

- In November 2024, the Organisation for Economic Co-operation and Development (OECD) Global Plastics Outlook reported that packaging contributes around 40% of global plastic waste, with 37% in the United States, 38% in Europe, and 45% in China. This collectively accounts for 60% of worldwide packaging waste generation.

This creates waste management issues and exposes manufacturers to regulatory pressure in regions with strict environmental standards. To address this challenge, manufacturers are developing recyclable or mono-material films that maintain barrier properties, introducing biodegradable and compostable alternatives, and implementing take-back or recycling programs in collaboration with converters and brand owners. These initiatives aim to reduce environmental impact while maintaining product performance.

- IIn July 2025, RDM Group partnered with Ecopol to develop a recyclable barrier board combining recycled cartonboard with PVOH functional barrier film. This innovation reduces reliance on virgin materials, lowers carbon footprint, and ensures full recyclability. It helps manufacturers meet strict environmental regulations, supports brand sustainability goals, and addresses growing consumer demand for eco-friendly packaging solutions.

Market Trend

Enhanced Protection and Multilayer Adoption

The global barrier films market is witnessing the growing adoption of multilayer and high-barrier films. These films combine multiple polymer layers or coatings to provide superior protection against oxygen, moisture, and light, ensuring extended shelf life and product integrity across food, pharmaceutical, and industrial applications.

The use of multilayer structures enables manufacturers to optimize barrier performance while maintaining flexibility and mechanical strength. Additionally, high-barrier films support sustainability initiatives by allowing mono-material constructions that improve recyclability. This trend reflects the increasing demand for advanced packaging solutions that balance product safety, durability, and environmental considerations.

Barrier Films Market Report Snapshot

|

Segmentation

|

Details

|

|

By Materials

|

Polyethylene (PE), Polyethylene Terephthalate (PET), Polypropylene (PP), Polyamides (PA), Ethylene Vinyl Alcohol (EVOH), Linear Low-Density Polyethylene (LLDPE), Others

|

|

By Type

|

Metalized Barrier Films, Transparent Barrier Films, White Barrier Films

|

|

By Layer

|

Multiple Layers, Single Layers

|

|

By Packaging Type

|

Pouches, Bags, Blister Packs

|

|

By End Use

|

Food and Beverage Packaging, Pharmaceutical Packaging, Agriculture, Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Materials (Polyethylene (PE), Polyethylene Terephthalate (PET), Polypropylene (PP), Polyamides (PA), and Ethylene Vinyl Alcohol (EVOH), Linear Low-Density Polyethylene (LLDPE), and Others): The polyethylene (PE) segment earned USD 12.41 billion in 2024, due to its widespread use in flexible packaging and cost-effectiveness for high-barrier applications.

- By Type (Metalized Barrier Films, Transparent Barrier Films, and White Barrier Films): The metalized barrier films segment held 48.13% of the market in 2024, due to superior moisture, oxygen, and light barrier properties suitable for food, pharmaceutical, and industrial packaging.

- By Layer (Multiple Layers and Single Layers): The multiple layers segment is projected to reach USD 32.23 billion by 2032, owing to enhanced barrier performance and protection for sensitive products.

- By Packaging Type (Pouches, Bags, and Blister Packs): The pouches segment is estimated to reach USD 27.66 billion by 2032, owing to the growing demand for convenient, lightweight, and easy-to-use packaging formats.

- By End Use (Food and Beverage Packaging, Pharmaceutical Packaging, Agriculture, and Others): The food and beverage packaging segment is anticipated to reach USD 23.39 billion by 2032, owing to the rising consumption of packaged and processed foods globally.

Barrier Films Market Regional Analysis

Based on region, the market has been classified into North America, Europe, Asia Pacific, the Middle East & Africa, and South America.

Asia Pacific accounted for a substantial market share of 34.43% in 2024, with a valuation of USD 12.79 billion. The region’s dominance is primarily driven by the rapid growth of packaged and processed food consumption across China, India, Japan, and Southeast Asian nations.

- In December 2024, the Consultative Group on International Agricultural Research (CGIAR) reported that 96.55% of households consumed packaged processed food in 2022–23, highlighting the widespread adoption of packaged food

Rising urbanization, increasing disposable incomes, and changing dietary patterns have fueled the demand for packaged foods, which boosts the need for high-performance barrier films to preserve freshness and extend shelf life. Additionally, the expansion of pharmaceutical and consumer goods manufacturing in the region supports the adoption of barrier films.

North America barrier films industry is expected to register the fastest growth in the market, with a projected CAGR of 5.04% over the forecast period. This growth is largely fueled by significant investments in the pharmaceutical industry, including the expansion of manufacturing facilities, R&D centers, and production of high-value medicines.

The presence of major pharmaceutical and healthcare companies, coupled with increasing production of sensitive drugs and biologics, drives the demand for advanced barrier films that provide superior protection against moisture, oxygen, and light. Furthermore, a mature processed food and convenience packaging market in the U.S. and Canada contributes to the region’s accelerated market growth.

- In July 2025, AstraZeneca announced a USD 50 billion investment in the U.S. by 2030, to expand its pharmaceutical manufacturing and R&D facilities, including a new drug substance manufacturing center in Virginia and multiple R&D and specialty manufacturing sites across the country.

Regulatory Frameworks

- In the United States, barrier films used in food and pharmaceutical packaging are regulated by the Food and Drug Administration (FDA), which sets standards for materials that come into contact with food and drugs to ensure safety, chemical migration limits, and compliance with the Food, Drug, and Cosmetic Act.

- In Europe, barrier films are governed under the European Food Safety Authority (EFSA) and must comply with the EU Framework Regulation, which ensures that materials in contact with food do not release harmful substances and maintain food safety.

- In China, the National Medical Products Administration (NMPA) and China Food and Drug Administration (CFDA) regulate barrier films used in pharmaceuticals and food packaging, focusing on safety, migration limits, and production standards.

- In Japan, the Ministry of Health, Labour and Welfare (MHLW) oversees the safety of barrier films used in food and pharmaceuticals, ensuring compliance with the Food Sanitation Act and Pharmaceutical and Medical Device Act.

- In India, barrier films for food and pharmaceutical applications are regulated by the Food Safety and Standards Authority of India (FSSAI) and the Central Drugs Standard Control Organization (CDSCO), which enforce standards for material safety, chemical migration, and manufacturing practices.

Competitive Landscape

Key players operating in the barrier films industry are focusing on various strategies to strengthen their market position and expand their product portfolios. They are forming strategic partnerships and collaborations, enabling companies to leverage technological expertise, enhance product offerings, and enter new regional markets efficiently.

Manufacturers are investing in advanced manufacturing facilities and expanding production capacity, which allows them to improve operational efficiency and meet growing demand across various end-use industries. These strategies help market participants maintain competitiveness and sustain long-term growth.

- In May 2025, Colorcon partnered with ASHA Cellulose to develop barrier membrane formulations for pharmaceutical and nutraceutical industries. The collaboration enhances regional market presence, accelerates product innovation, and provides high-performance, sustainable packaging solutions. It helps manufacturers meet regulatory requirements, improve product protection, and address growing demand for durable and eco-friendly packaging across multiple regions.

Key Companies in Barrier Films Market:

- Amcor plc

- Sealed Air

- Mondi

- Cosmo Films

- TEIJIN LIMITED

- TOPPAN Inc.

- Huhtamäki Oyj

- Winpak LTD.

- Celplast Metallized Products

- C. Jindal group

- Glenroy, Inc.

- Toray Industries, Inc.

- Schur Hagen & Sivertsen

- FLAIR Flexible Packaging Corporation

- HPM GLOBAL

Recent Developments (Product Launches/Collaboration)

- In June 2025, Mondi launched the re/cycle PaperPlus Bag Advanced, a high-performance and recyclable paper bag with a thin barrier film that protects humidity-sensitive products, reduces plastic use by up to 60%, lowers carbon footprint, maintains product integrity, and supports seamless integration with existing filling and sealing lines.

- In April 2025, Toyo Seikan Group Holdings launched the MiraNeo functional materials brand and developed Ultra Moisture Barrier Film, targeting flexible solar power panels to enhance moisture protection, durability, and support greenhouse gas emission reduction.

- In September 2024, Henkel collaborated with Panverta to develop mono-material polypropylene films with improved oxygen barrier properties for sustainable dry food packaging.