Cold chain equipment comprises temperature-controlled devices and systems used to store, transport, and distribute temperature-sensitive products such as vaccines, biopharmaceuticals, food, and chemicals.

It includes refrigerators, freezers, cold boxes, insulated containers, and refrigerated transport vehicles designed to maintain product integrity throughout the supply chain. The equipment ensures products remain within a specified temperature range from production to end use, preserving their quality, efficacy, and safety.

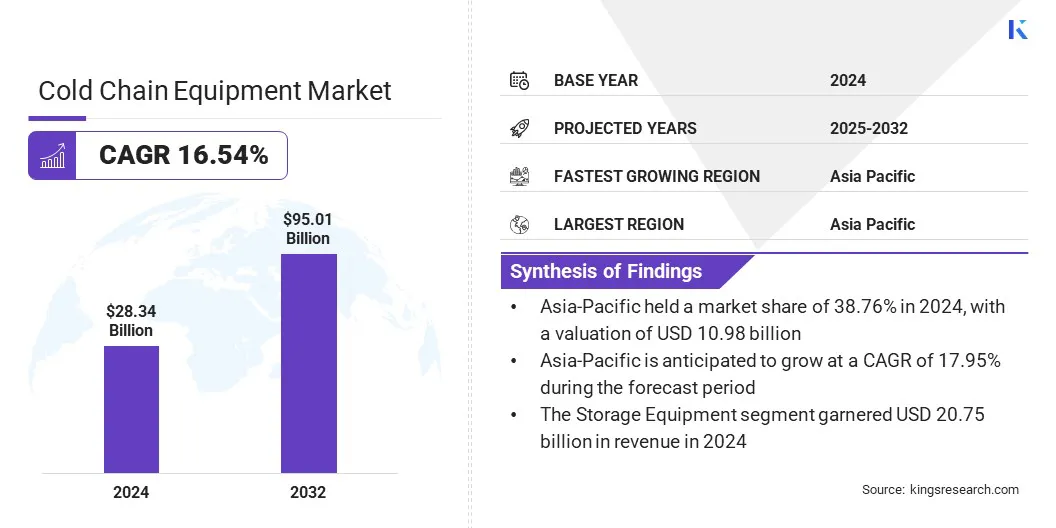

Cold Chain Equipment Market Overview

The global cold chain equipment market size was valued at USD 28.34 billion in 2024 and is projected to grow from USD 32.54 billion in 2025 to USD 95.01 billion by 2032, exhibiting a CAGR of 16.54% during the forecast period.

The market is witnessing steady growth, mainly driven by increasing demand for temperature-sensitive pharmaceuticals, vaccines, and perishable food products. Advancements in refrigeration technologies and stricter regulatory standards further support market expansion.

Key Highlights:

The cold chain equipment industry size was recorded at USD 28.34 billion in 2024.

The market is projected to grow at a CAGR of 16.54%from 2025 to 2032.

North America held a share of 30.11% in 2024, valued at USD 8.53 billion.

The storage equipment segment garnered USD 20.75 billion in revenue in 2024.

The food & beverages segment is expected to reach USD 50.45 billion by 2032.

Asia Pacific is anticipated to grow at a CAGR of 17.95% over the forecast period.

Major companies operating in the cold chain equipment market are Thermo King, Carrier, Emerson Electric Co, Danfoss, BITZER Kühlmaschinenbau GmbH, GEA Group, Kelvion Holding GmbH, CAREL INDUSTRIES S.p.A., Rivacold srl, Viessmann Refrigeration Solutions GmbH, Haier Biomedical, Blue Star Limited, Schmitz Cargobull, Krones, and HYUNDAI TRANSLEAD.

The market is influenced by rising demand for temperature-controlled storage and transportation across the food, pharmaceutical, and perishable goods sectors. Increasing government focus on reducing food loss, enhancing food safety, and promoting sustainable infrastructure is further fueling adoption. Advances in energy-efficient and solar-powered cold storage solutions are also supporting market expansion by addressing operational costs and environmental concerns.

In 2025, the United Nations Capital Development Fund (UNCDF) and the United Nations Development Programme (UNDP) announced a joint initiative to expand solar-powered cold storage infrastructure across Kenya, aiming to reduce spoilage, support over 60,000 smallholder farmers, and avoid 4.8 billion tonnes of CO₂ equivalent emissions by 2034.

What is driving the growing demand for cold chain equipment across healthcare and food supply chains?

A key factor propelling the growth of the cold chain equipment market is the rising need to maintain product integrity across temperature-sensitive supply chains. The expanding pharmaceutical and biotechnology industries are creating a strong demand for reliable cold storage and transportation systems to preserve the potency of vaccines, biologics, and specialty drugs.

Moreover, the growing global trade of perishable food products requires efficient temperature control to prevent spoilage and comply with stringent food safety standards. This increasing reliance on temperature-regulated logistics and storage solutions is fueling widespread adoption of advanced cold chain equipment across healthcare and food sectors.

In 2024, UNICEF delivered 2.787 billion vaccine doses to 99 countries, reaching 45% of the world’s children under 5. To support this, UNICEF procured 1,500 solar systems to power medical equipment and vaccine storage facilities, enhancing cold chain infrastructure in underserved regions.

What key factors related to capital and operational costs are hindering the growth of the cold chain equipment market?

A key challenge impeding the progress of the market is the high capital and operational costs associated with advanced refrigeration systems. Manufacturing and deploying energy-efficient, IoT-enabled, and temperature-controlled units require significant upfront investment, along with specialized maintenance and a skilled workforce, which raises overall operational expenses. These cost constraints hinder adoption, particularly among small and medium-sized logistics providers, limiting large-scale deployment of cold chain solutions.

To address this challenge, market players are investing in energy-efficient technologies, modular system designs, and predictive maintenance solutions to reduce operating costs. They are also optimizing supply chains, adopting local sourcing strategies, and forming strategic partnerships to improve cost efficiency and enhance market accessibility.

How is the integration of smart and automated technologies shaping the cold chain equipment market?

A key trend influencing the market is the growing adoption of smart and automated systems. Manufacturers are integrating IoT-enabled sensors, real-time temperature monitoring, and automated alert mechanisms to enhance storage precision, traceability, and operational efficiency.

These innovations minimize product spoilage, ensure compliance with stringent regulatory standards, and improve reliability across pharmaceutical, food, and biotech supply chains. The deployment of advanced cold chain equipment is fueling wider adoption among hospitals, laboratories, and commercial logistics operations.

In October 2024, Carrier Transicold unveiled its next-generation Supra A and Citimax D series refrigeration units at REFCOLD 2024 in Kolkata, India, highlighting advanced technology and enhanced efficiency solutions for the cold chain sector.

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

South America: Brazil, Argentina, Rest of South America

Market Segmentation

By Equipment Type (Storage Equipment and Transportation Equipment): The storage equipment segment earned USD 20.75 billion in 2024, mainly due to rising demand for temperature-controlled storage solutions across the food, pharmaceutical, and logistics sectors.

By Application (Food & Beverages, Pharmaceuticals, Chemicals, and Others): The food & beverages segment held a share of 52.11% in 2024, largely attributed to increasing demand for refrigerated storage and transportation to preserve perishable goods and reduce spoilage across the supply chain.

What is the market scenario in Asia-Pacific and North America region?

Based on region, the global cold chain equipment market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

Asia Pacific cold chain equipment market share stood at 38.76% in 2024, valued at USD 10.98 billion. This dominance is reinforced by the rapid expansion of e-commerce, pharmaceutical distribution, and perishable food supply chains across the region.

Countries such as China, India, Japan, and South Korea are investing heavily in modern logistics infrastructure, including temperature-controlled warehouses and last-mile delivery systems, to maintain product integrity and meet regulatory standards.

Governments in the region are also making investments in cold storage facilities and offering incentives to modernize the food and pharmaceutical supply chains, boosting regional market expansion. Strategic partnerships between local logistics providers, technology companies, and government initiatives promoting cold chain modernization are accelerating adoption and supporting regional market expansion.

In June 2025, the Philippine government allocated USD 53 billion to establish around 100 cold storage facilities aimed at extending the shelf life of fruits, vegetables, and other high-value crops. This initiative reflects the government’s strategic commitment to strengthening the nation’s cold chain logistics infrastructure and ensuring the quality and safety of perishable goods.

North America cold chain equipment industry is poised to grow at a robust CAGR of 16.33% over the forecast period. This growth is supported by the growing demand for temperature-sensitive pharmaceuticals, biologics, and perishable food products.

The regional market further benefits from a well-established logistics infrastructure, advanced refrigeration technologies, and strong regulatory enforcement by agencies such as the U.S. Food and Drug Administration (FDA) and the U.S. Department of Agriculture (USDA), which mandate strict cold chain compliance.

Additionally, increased government and private sector investments in cold storage capacity, particularly to support vaccine distribution and frozen food exports, are fueling domestic market expansion. Additionally, manufacturers are prioritizing sustainability through the adoption of energy-efficient refrigeration systems and low-GWP refrigerants, aligning with North American climate policies.

Regulatory Frameworks

In North America, the U.S. Food and Drug Administration (FDA) and the U.S. Department of Agriculture (USDA) regulate cold chain equipment and storage facilities to ensure food safety and compliance with temperature control standards. The Food Safety Modernization Act (FSMA) further enforces preventive controls for temperature-sensitive products.

In Europe, the European Food Safety Authority (EFSA) sets guidelines for cold storage and transport, complemented by EU regulations on food hygiene (Regulation (EC) No 852/2004) to maintain product quality and safety.

In China, the National Health Commission (NHC) and Ministry of Agriculture enforce standards for refrigerated storage and transport of food and pharmaceuticals, including mandatory temperature monitoring.

Globally, the Codex Alimentarius Commission provides international guidance on food storage and transport standards, promoting harmonization and best practices across borders.

Competitive Landscape

Leading players in the cold chain equipment industry are focusing on technological innovation, capacity expansion, and strategic collaborations. Manufacturers are investing in energy-efficient, modular, and solar-powered refrigeration units to improve operational efficiency and sustainability.

Companies are also expanding production facilities and distribution networks across high-growth regions to meet rising demand for temperature-controlled storage solutions. Additionally, partnerships with logistics providers, food processors, and governments support integrated cold chain solutions, strengthen market presence, and accelerate adoption across the food, pharmaceutical, and perishable goods sectors.

In May 2025, Thermo King introduced its latest electric and hybrid transport refrigeration units (TRUs) at ACT Expo 2025, including the fully electric A-500e for long-haul trailers, and the Precedent S-750i hybrid-electric model. These units are designed to reduce emissions and fuel consumption while enhancing operational efficiency.

In August 2024, Trane Technologies plc, under its Thermo King brand, acquired Klinge Corporation to strengthen its sustainable transport temperature control portfolio. Klinge Corporation, a specialist in ISO refrigerated containers, broadens Thermo King's range of solutions for transporting temperature-sensitive products, supporting the company’s growth strategy and reinforcing its commitment to efficient global cold chain operations.

In February 2025, Carrier Transicold introduced the Vector S 15, a next-generation trailer refrigeration unit engineered to optimize total cost of ownership in cold chain logistics. The unit incorporates Carrier’s E-Drive all-electric technology, which eliminates mechanical transmissions and belts, thereby reducing maintenance requirements and enhancing operational reliability.

freqAskQues

What is the projected growth of the cold chain equipment market?

What are the main drivers of demand for cold chain equipment?

Which types of cold chain equipment are most used?

Which regions are leading adoption of cold chain equipment?

What challenges does this market face?

Who are some major players in this space?

What innovations are shaping the cold chain equipment market?

What opportunities exist for investors and developers?

How can this report help me understand the long-term financial benefits of investing in cold chain equipment?

How does this report address my concern about equipment failing to maintain optimal temperatures?

How can this report help me justify investment in large-scale cold storage facilities?

How does this report help me understand the latest technologies to improve cold chain efficiency?

Author

Swati is a committed research analyst with a passion for optimizing systems and processes across industries, specializing in healthcare but also bringing valuable expertise to sectors such as consumer goods, life sciences, and more. Her cross-domain research approach allows her to generate clear, actionable reports that inform strategic decisions in a variety of fields. Swati is committed to staying ahead of evolving trends, leveraging her broad understanding of different sectors to provide insights that are relevant to a range of industries. In her personal time, she enjoys music and spending quality time with her family, which inspires her creativity and enriches her professional approach.

With over a decade of research leadership across global markets, Ganapathy brings sharp judgment, strategic clarity, and deep industry expertise. Known for precision and an unwavering commitment to quality, he guides teams and clients with insights that consistently drive impactful business outcomes.

Cold Chain Equipment Market

Cold Chain Equipment Market