Pea Starch Market Size, Share, Growth & Industry Analysis, By Type (Industrial, Food, Feed), By End Use (Food & Beverage, Paper, Pharmaceuticals, Others), and Regional Analysis, 2025-2032

pages: 140 | baseYear: 2024 | release: November 2025 | author: Sunanda G. | lastUpdated: November 2025

The market encompasses the production and utilization of starch extracted from yellow peas, a natural carbohydrate recognized for its thickening, gelling, and binding capabilities. Pea starch serves as a functional ingredient across diverse formulations owing to its gluten-free and clean-label characteristics.

It finds broad applications in food and beverages, pharmaceuticals, animal feed, and industrial sectors, where it supports performance, stability, and formulation consistency. The market analysis covers segmentation based on type, end use, and regional distribution to provide insights into key growth areas and emerging opportunities.

Pea Starch Market Overview

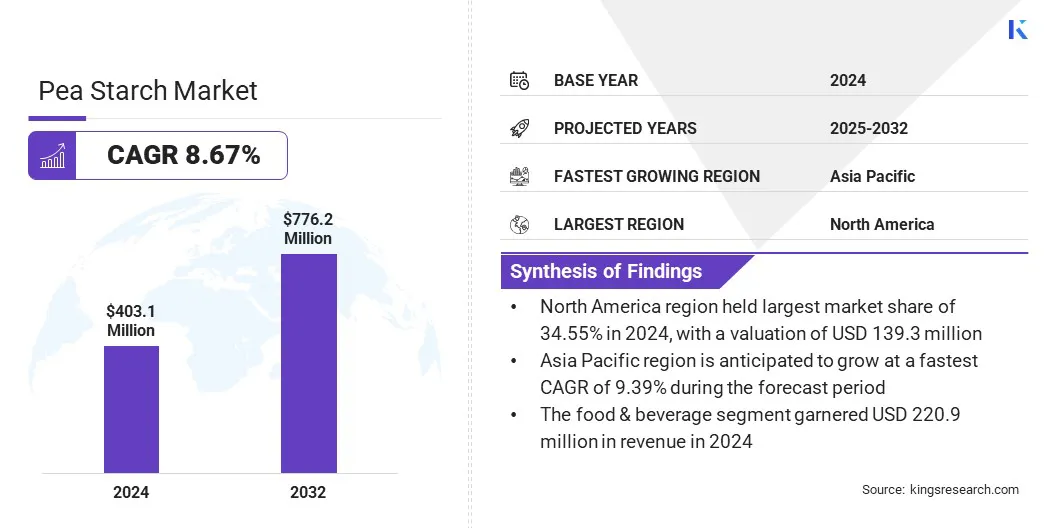

The global pea starch market size was valued at USD 403.1 million in 2024 and is projected to grow from USD 433.8 million in 2025 to USD 776.2 million by 2032, exhibiting a CAGR of 8.67% over the forecast period.

The growth is due to the rising consumer preference for allergen-free and clean-label ingredients in bakery, snacks, and processed foods, which is increasing the demand for gluten-free pea starch. Manufacturers in the pharmaceutical and nutraceutical sectors are increasingly replacing traditional gelatin with pea starch to produce vegetarian and allergen-free softgel capsules that meet regulatory and quality standards.

Key Highlights:

The pea starch industry size was recorded at USD 403.1 million in 2024.

The market is projected to grow at a CAGR of 8.67% from 2025 to 2032.

North America held a market share of 34.55% in 2024, with a valuation of USD 139.3 million.

The industrial segment garnered USD 182.3 million in revenue in 2024.

The food & beverage segment is expected to reach USD 427.1 million by 2032.

Asia Pacific is anticipated to grow at a CAGR of 9.39% over the forecast period.

Major companies operating in the pea starch market are Ingredion, Roquette Frères, Emsland Group, COSUCRA, The Scoular Company, Puris, Nutri-Pea, Vestkorn, Meelunie B.V., Dakota Ingredients, P&H Milling, Inc., Farbest Brands, Ebro Foods, S.A., Laybio, and Makendi WorldWide.

Companies are developing pea starch-based solutions that improve texture, stability, and shelf life in processed and convenience foods. These innovations are provided to meet the growing demand for ready-to-eat meals, snacks, and baked products that require consistent quality and functional performance.

The expansion of pea starch applications in these food categories enhances product versatility and allows manufacturers to cater to consumer preferences for convenient and high-quality ingredients. This approach supports broader utilization of pea starch across the food industry and contributes to market growth.

How is the growing demand for gluten-free products driving the market?

The global pea starch market is experiencing significant growth due to the increasing demand for gluten-free products. Consumers with gluten intolerance and celiac disease are seeking alternatives to wheat- and barley-based ingredients, which has created a strong need for gluten-free solutions in food production.

Pea starch serves as an effective substitute because it provides similar functional properties, such as thickening, gelling, and stabilizing, while remaining naturally gluten-free. This rising consumer preference encourages food manufacturers to incorporate pea starch into bakery products, snacks, and other gluten-free formulations.

How is the limited availability of high-quality peas slowing market growth?

The limited availability of high-quality peas is a major challenge in the pea starch market, which affects the consistency and yield of starch production. Variations in crop quality due to weather conditions, soil fertility, and seasonal fluctuations make it difficult for manufacturers to maintain uniform product quality. This constraint can impact production efficiency and restrict market growth.

To address this challenge, companies are collaborating with farmers to implement improved cultivation practices and select pea varieties with higher starch content. Additionally, adopting advanced processing techniques helps optimize starch extraction and maintain consistent product quality.

What are the major trends in this market?

The global pea starch market is witnessing a growing adoption of pea starch-based softgel capsules in the pharmaceutical and nutraceutical sectors. Manufacturers are increasingly replacing traditional gelatin with pea starch to produce vegetarian and allergen-free capsules. This shift is driven by rising consumer demand for clean-label and plant-based products.

In May 2024, Roquette launched its LYCAGEL Flex hydroxypropyl pea starch premix for nutraceutical and pharmaceutical softgel capsules. The premix provides manufacturers with a plant-based alternative to gelatin, allowing customization of plasticizer combinations for various capsule formulations. It offers reduced degassing time, easy equipment cleaning, and maintains mechanical strength, stability, and appearance over six months of storage.

Pea Starch Market Report Snapshot

Segmentation

Details

By Type

Industrial, Food, Feed

By End Use

Food & Beverage, Paper, Pharmaceuticals, Others

By Region

North America: U.S., Canada, Mexico

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

South America: Brazil, Argentina, Rest of South America

Market Segmentation:

By Type (Industrial, Food, and Feed): The industrial segment earned USD 182.3 million in 2024, due to increasing use of pea starch in biodegradable packaging, adhesives, and textile applications where sustainable raw materials are gaining preference.

By End Use (Food & Beverage, Paper, Pharmaceuticals, and Others): The food & beverage segment held 45.23% of the market in 2024, due to rising demand for clean-label and gluten-free ingredients in processed foods, bakery products, and snacks.

What is the market scenario in North America and Asia-Pacific region?

Based on region, the global pea starch market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

North America pea starch market share stood around 34.55% in 2024 in the global market, with a valuation of USD 139.3 million. The dominance is driven by processing plants expansion and private sector investments in advanced food ingredient manufacturing facilities across the U.S. and Canada.

These investments focus on scaling the production of gluten-free and plant-based ingredients for bakery, snack, and meat alternative applications. Increased production capacity improves product availability and efficiency, reinforcing North America’s dominance in the market.

In November 2024, Roquette announced plans to expand its pea processing plant in Portage la Prairie, Manitoba, to double its current production capacity. The USD 600 million facility, which produces pea protein, food-grade starches, and other components, will receive new equipment funded in part through the Sustainable Canadian Agriculture Partnership.

Asia Pacific is poised to grow at a significant CAGR of 9.39% over the forecast period. The growth is driven by government initiatives promoting domestic pulse processing industries in countries such as China and India. These programs support the use of locally grown peas for starch extraction and provide incentives for private sector investments in processing plants.

Expansion of manufacturing capabilities improves production efficiency, ensures a consistent supply, and reduces dependency on imports. Increasing availability of pea starch encourages its adoption in food, pharmaceutical, and industrial applications, thereby driving market growth across the region.

Regulatory Frameworks

In the U.S, the Food and Drug Administration (FDA) regulates food ingredients, including pea starch, under the Federal Food, Drug, and Cosmetic Act. The FDA oversees the safety of food ingredients and additives, ensuring they are safe for consumption. Pea starch used in food products must comply with FDA regulations to be marketed in the U.S.

In Europe, Regulation (EC) No 1333/2008 governs the use of food additives, including those derived from pea starch. This regulation sets out rules for the authorization and use of food additives in foods, aiming to ensure a high level of protection of human health and consumer interests. It includes provisions for the evaluation of food additives, labeling requirements, and the establishment of acceptable daily intakes.

In India, the Food Safety and Standards Authority of India (FSSAI) regulates pea starch under the Food Safety and Standards (Food Products Standards and Food Additives) Regulations, 2011. These regulations establish standards for food products, including starches, to ensure their safety and quality. The FSSAI mandates compliance with specific requirements related to labeling, packaging, and permissible additives for pea starch products.

In Japan, the Ministry of Health, Labour and Welfare (MHLW) oversees food safety regulations, including those applicable to pea starch. The Food Sanitation Act and related regulations set standards for food additives, contaminants, and labeling. These regulations ensure that pea starch products meet safety and quality standards before entering the Japanese market.

Competitive Landscape

Key players in the pea starch industry are actively pursuing strategic investments and forming partnerships to strengthen their capabilities in manufacturing new ingredients and food products.

Companies are also entering into strategic collaborations with industry peers, suppliers, and research institutions. These partnerships aim to co-develop new ingredients and food products, combining expertise to accelerate innovation and bring differentiated offerings to the market. These efforts are enabling companies to expand their product portfolios, optimize manufacturing capabilities, and strengthen their position in the market.

In July 2025, Protein Industries Canada announced a new pilot project in partnership with Louis Dreyfus Company (LDC) and the Chronic Disease Innovation Centre (CDIC) to develop pea-protein ingredients and finished food products. The project involves a commitment of approximately USD 34.7 million and focuses on producing a pea protein isolate in a new facility in Yorkton, Saskatchewan, by the end of 2025.

In June 2024, Bunge expanded its portfolio to include pea and faba protein concentrates through a collaboration with Golden Fields in Latvia. The new range includes non-GMO, finely powdered protein concentrates with 55-70% protein content for food, pet, and feed applications. The products are extracted via dry-fractionation, supporting sustainable practices and reducing water and solvent use.

freqAskQues

What is the projected growth of the pea starch market?

Which factors are driving the adoption of pea starch solutions?

What are the major challenges limiting the growth of the pea starch market?

Who are the key players operating in the global market?

Which trends are shaping the market?

Which regions are leading in pea starch adoption, and why?

What are the most in-demand end uses of pea starch?

How are regulatory frameworks impacting pea starch globally?

How can this report help me explain the benefits of pea starch solutions to my clients?

How does this report help me understand the competitive landscape and identify potential partners in pea starch?

The report provides insights into key players, their strategic investments, partnerships, and product offerings. It enables benchmarking, identification of collaborators, and evaluation of opportunities to co-develop ingredients and food products.

How does this report help me understand the key challenges and risks in pea starch?

Author

Sunanda is a proficient research analyst with strong cross-domain expertise, excelling in identifying market trends and delivering insightful analyses across various industries, including consumer goods, food & beverages, healthcare, and more. Her ability to connect insights from diverse sectors enables her to offer actionable recommendations that support strategic decision-making in a range of business contexts. Sunanda’s research is driven by thorough data analysis and her commitment to providing relevant, data-driven insights. Outside of her professional endeavors, Sunanda's passion for travel, adventure, and music fuels her creativity and broadens her perspective, enriching her approach to both life and work.

With over a decade of research leadership across global markets, Ganapathy brings sharp judgment, strategic clarity, and deep industry expertise. Known for precision and an unwavering commitment to quality, he guides teams and clients with insights that consistently drive impactful business outcomes.

Pea Starch Market

Pea Starch Market