pages: | baseYear: | release: | author: | lastUpdated:

enquireNow

pages: | baseYear: | release: | author: | lastUpdated:

Compressed natural gas (CNG) powertrain systems utilize natural gas as the primary fuel source to operate engines with reduced environmental impact. These systems integrate engines, fuel tanks, injectors, transmissions, exhaust systems, and control units to ensure efficient and reliable vehicle performance.

They are deployed across passenger, light, and heavy commercial vehicles, as well as specialized fleets in transportation, logistics, and industrial sectors, supporting energy diversification and regulatory compliance in emission reduction.

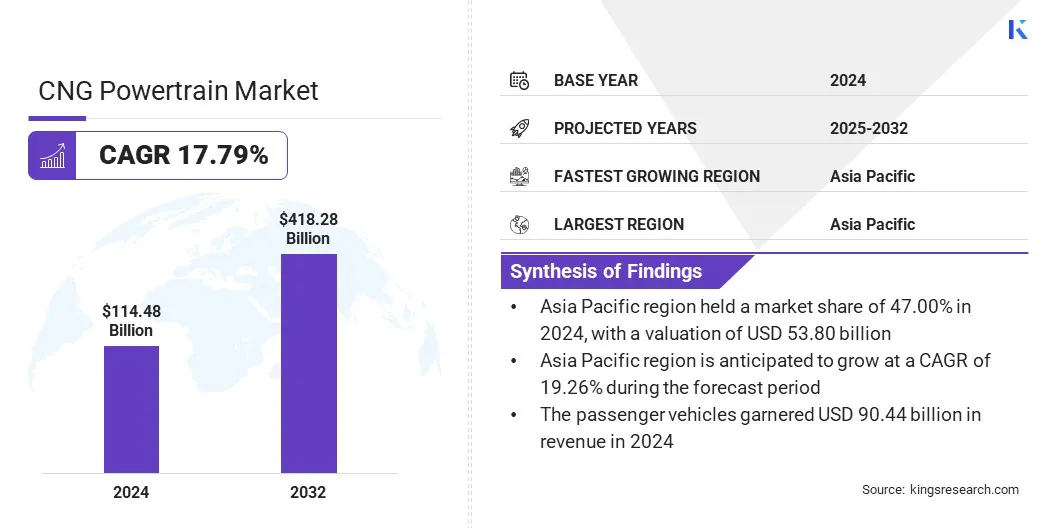

According to Kings Research, the global CNG powertrain market size was valued at USD 114.48 billion in 2024 and is projected to grow from USD 132.94 billion in 2025 to USD 418.28 billion by 2032, exhibiting a CAGR of 17.79% during the forecast period.

This growth is fueled by the growing demand for fuel-efficient vehicles, as rising fuel costs and environmental concerns accelerate the shift toward alternative fuel technologies. Advancements in turbocharged CNG engines are further improving vehicle performance, fuel efficiency, and emission control, strengthening the competitiveness of CNG vehicles against conventional engines.

Major companies operating in the CNG powertrain market are Robert Bosch GmbH, Shigan Quantum Technologies Limited, Cummins Inc., AB Volvo, Hyundai Motor Company, Maruti Suzuki India Limited, Iveco Group Company, Scania, Renault Group, TATA Motors, HINDUJA GROUP, Mahindra&Mahindra Ltd., Volkswagen, Ford Motor Company, and Allison Transmission, Inc.

Companies are developing integrated CNG powertrain solutions and optimized refueling strategies for fleet operations, including buses, taxis, and commercial delivery vehicles. These solutions are being provided to meet the growing demand for cleaner and cost-efficient fuel alternatives in fleet transportation.

The adoption of CNG-powered fleets is improving operational efficiency, reducing fuel costs, and lowering emissions in urban and intercity transport networks. This approach is promoting broader deployment of CNG vehicles across the commercial sector.

Growing Demand for Fuel-Efficient Vehicles

The expansion of the CNG powertrain market is fueled by the increasing demand for fuel-efficient vehicles. Rising fuel costs and environmental concerns are prompting consumers and fleet operators to adopt vehicles with higher mileage and lower operating expenses.

CNG powertrains provide a cost-effective alternative to conventional petrol and diesel engines by delivering better fuel efficiency and reduced carbon emissions. This growing preference for economical and sustainable transportation solutions is boosting the adoption of the CNG powertrain across both passenger and commercial vehicle segments.

High Initial Cost of CNG Powertrain Systems

A significant challenge impeding the expansion of the CNG Powertrain market is the high upfront cost of CNG engines and associated components compared to conventional fuel systems. This cost barrier discourages small and mid-sized vehicle manufacturers and fleet operators from adopting CNG technology.

To mitigate this challenge, companies are reducing costs through modular engine designs and large-scale production. Moreover, governments are offering subsidies and incentives to make CNG vehicles more affordable and boost wider adoption.

Development of Turbocharged CNG Engines

The CNG powertrain market is witnessing a notable trend toward the development of turbocharged CNG engines. Manufacturers are improving these engines to enhance performance, fuel efficiency, and emission control.

These advancements enable CNG vehicles to achieve power levels comparable to conventional engines, increasing their applicability in both passenger and commercial segments. Enhanced engine efficiency also extends vehicle range and lowers operating costs, supporting wider adoption of CNG powertrains across urban and intercity transportation networks.

|

Segmentation |

Details |

|

By Component |

Engine, Fuel Injector, Transmission, Fuel Tank, Exhaust System, Control Unit |

|

By Vehicle Type |

Passenger Vehicles (Sedans, Hatchbacks, SUVs), Commercial Vehicles (Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV)) |

|

By Drive Type |

Front Wheel Drive (FWD), Rear Wheel Drive (RWD), All-Wheel Drive (AWD) |

|

By Fuel Type |

Mono-fuel, Bi-fuel |

|

By Application |

Transportation, Logistics, Industrial |

|

By Region |

North America: U.S., Canada, Mexico |

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe | |

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific | |

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa | |

|

South America: Brazil, Argentina, Rest of South America |

Based on region, the global market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

Asia Pacific CNG powertrain market share stood at 47.00% in 2024, valued at USD 53.80 billion. This dominance is reinforced by robust infrastructure development and government initiatives supporting CNG refueling stations.

Extensive networks of CNG stations in countries such as India and China are enabling wider adoption of CNG vehicles in both passenger and commercial segments. These measures are increasing vehicle accessibility and fueling convenience, which is driving continued demand for CNG powertrains and reinforcing the region’s market dominance.

The Europe CNG powertrain industry is poised to grow at a significant CAGR of 17.51% over the forecast period. The growth is propelled by the strong adoption of CNG in public transport systems across major cities. Governments and municipal authorities are investing in expanding CNG bus fleets and upgrading refueling infrastructure to meet emission reduction targets.

These initiatives are boosting demand for CNG powertrain components and prompting manufacturers to increase production capacity and develop advanced engines, positioning Europe as a key market for or CNG powertrains.

Key players in the global CNG powertrain market are forming strategic collaborations to advance hybrid and combustion powertrain components and systems. Companies are engaging in joint research and development programs to co-design CNG-adapted engines and hybrid control software.

Manufacturers are entering co-development agreements to integrate CNG storage modules with transmission and exhaust architectures. Companies are establishing supplier-OEM partnerships to align component specifications and accelerate production readiness. They are forming joint ventures for shared manufacturing of high-pressure fuel tanks and control units.

freqAskQues