pages: | baseYear: | release: | author: | lastUpdated:

enquireNow

pages: | baseYear: | release: | author: | lastUpdated:

Biofortification is the process of increasing the nutritional value of staple crops by enhancing essential vitamins and minerals such as iron, zinc, and vitamin A during growth. It is achieved through selective breeding, agronomic practices, and biotechnological methods. The market includes the development, production, and distribution of nutrient-enriched seeds, along with their adoption by farmers and agricultural organizations to promote healthier crop outputs.

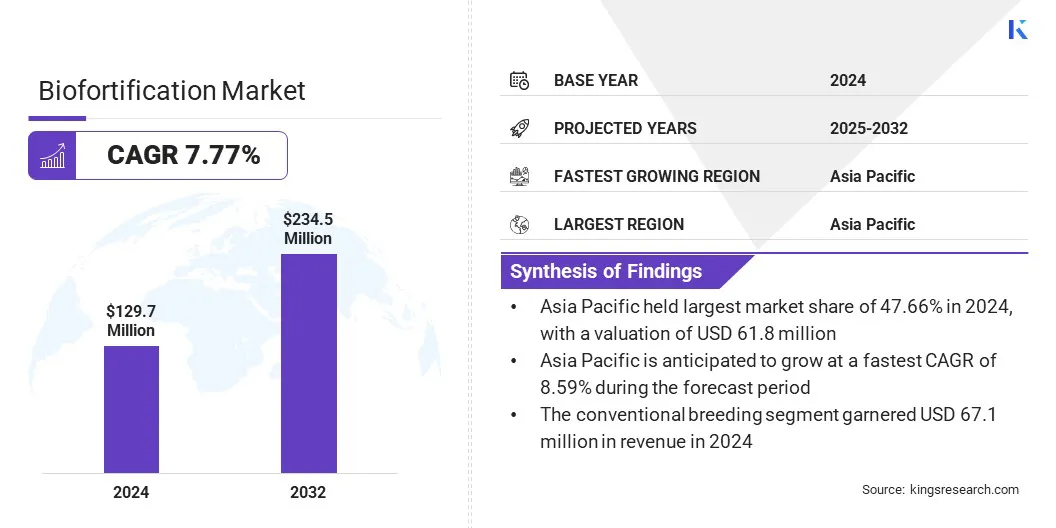

The global biofortification market size was valued at USD 129.7 million in 2024 and is projected to grow from USD 138.9 million in 2025 to USD 234.5 million by 2032, exhibiting a CAGR of 7.77% during the forecast period.

The market is expanding as rising awareness of micronutrient deficiencies creates a strong demand for nutrient-enriched staple crops. Government initiatives and public-private programs support the development and distribution of fortified seeds, while advances in plant breeding and biotechnology enhance nutrient content.

Major companies operating in the biofortification market are Cargill, Incorporated, UPL, JK Agri Genetics Limited, Better Nutrition, Nestlé, CATO FOODS, Syngenta Crop Protection AG, and Quemems farms.

Companies are investing in genome-editing technologies to enhance crop productivity and nutritional quality. Collaborations between private firms and agricultural research organizations focus on herbicide-tolerant, drought-resistant, and weed-controlled varieties while increasing micronutrient content in staples such as sorghum, rice, and wheat. Integrating nutrient-enriched traits influences the market, improves food security, mitigates hidden hunger, and promotes the adoption of nutrient-rich crops.

Rising Nutritional Deficiencies Globally

The biofortification market is experiencing significant growth, fueled by rising nutritional deficiencies worldwide. Inadequate intake of essential vitamins and minerals highlights a critical need for nutrient-rich crops. This shortage intensifies the demand for solutions that enhance dietary quality and support public health objectives.

Governments in countries such as India and Kenya, and organizations, including the World Health Organization and the Food and Agriculture Organization, increasingly prioritize interventions that combat malnutrition. Their support fuels investment and adoption in biofortification technologies, enabling scalable strategies to improve nutritional security and address global micronutrient gaps effectively.

Regulatory Resistance in Crop Enhancement

A significant challenge hindering the expansion of the biofortification market is the strong regulatory scrutiny and limited public acceptance of genetically modified approaches. Many regions enforce strict approval processes for GM crops, which significantly delay product launches and increase compliance costs. Additionally, consumer skepticism regarding GM foods can limit market penetration, affect adoption rates, and constrain the overall growth of biofortified crops.

To address this challenge, market players are increasingly prioritizing non-GM routes, including conventional breeding and marker-assisted selection, to ensure regulatory compliance and maintain consumer trust. These approaches also enable faster development and wider distribution of nutrient-enriched crops, supporting market growth.

Advancements in Precision Breeding and Crop Enhancement

The biofortification market is witnessing a notable trend toward advancements in precision breeding and crop enhancement, leading to the development of nutrient-enriched crops. Modern techniques, including genome editing and advanced agronomic practices, streamline the modification of crop traits with greater precision and efficiency.

These innovations improve operational processes by shortening cultivation cycles and enhancing yield reliability while ensuring elevated micronutrient content in staple crops. Adoption of these technologies fosters innovation in research and development pipelines. It allows companies to respond quickly to global nutritional needs and evolving consumer demands, influencing the market.

|

Segmentation |

Details |

|

By Crop type |

Rice, Corn, Cassava, Wheat, Beans, Others |

|

By Nutrient type |

Vitamins, Iron, Zinc, Amino Acids, Others |

|

By Technology |

Conventional Breeding, Agronomic Biofortification, Genetic Modification, Others |

|

By Region |

North America: U.S., Canada, Mexico |

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe | |

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific | |

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa | |

|

South America: Brazil, Argentina, Rest of South America |

Based on region, the market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

Asia Pacific biofortification market share stood at around 47.66% in 2024, valued at USD 61.8 million. This dominance is attributed to the region’s high prevalence of micronutrient deficiencies, particularly iron, zinc, and vitamin A, which has created significant demand for biofortified staple crops. Strong government initiatives, such as the National Nutrition Strategy in India and social safety-net programs in Bangladesh, are further accelerating adoption.

According to the World Bank, hidden hunger causes annual GDP losses of USD 12 billion in India, USD 3 billion in Pakistan, and USD 700 million in Bangladesh, prompting governments to prioritize cost-effective nutritional interventions such as biofortification. These factors, combined with support from international organizations and regional agricultural research institutions, position Asia Pacific as the leading hub for biofortification.

The Europe biofortification industry is expected to register the fastest growth, with a CAGR of 7.04% over the forecast period. This growth is propelled by substantial investments in research and development, along with the development of specialized laboratories and manufacturing facilities for biofortified crops.

Supportive policies from European governments promoting nutrition security, food quality, and sustainable agricultural practices further boost adoption. Additionally, rising consumer demand for nutrient-enriched and functional foods is prompting food manufacturers and farmers to integrate biofortified crops into supply chains, supporting regional market growth.

Key players in the biofortification industry are focusing on partnerships and research & development (R&D) initiatives to strengthen their market position and foster innovation. Companies are investing significantly in R&D to develop high-yield, nutrient-enriched, and climate-resilient crop varieties, while also improving seed technology and crop bioavailability.

Companies are also forming strategic collaborations with government agencies, international research organizations, and agricultural institutes to enhance the development, testing, and distribution of biofortified crops. By leveraging these strategies, key players are expanding their product portfolios, accelerating commercialization, and maintaining a competitive edge.

freqAskQues