Buy Now

CT and MRI Contrast Agents Market

CT and MRI Contrast Agents Market Size, Share, Growth & Industry Analysis, By Product (Gadolinium-based Contrast Media, Iodinated Contrast Media), By Modality (Magnetic Resonance Imaging, X-ray/ Computed Tomography), By Application, By Route of Administration, By End Use, and Regional Analysis, 2024-2031

Pages: 230 | Base Year: 2023 | Release: March 2025 | Author: Versha V.

Market Definition

The market encompasses the research, production, and commercialization of contrast agents used in medical imaging. It includes various types of contrast agents such as iodinated and gadolinium-based, along with distribution channels, regulatory considerations, and technological innovations.

The market also covers applications in hospitals, diagnostic imaging centers, and research, focusing on enhancing diagnostic accuracy and improving patient outcomes.

CT and MRI Contrast Agents Market Overview

The global CT and MRI contrast agents market size was valued at USD 5.98 billion in 2023 and is projected to grow from USD 6.47 billion in 2024 to USD 11.59 billion by 2031, exhibiting a CAGR of 8.70% during the forecast period. This market is registering substantial growth, fueled by continuous advancements in medical imaging technologies, which are enhancing the precision and effectiveness of diagnostic procedures.

Healthcare systems around the world are increasingly emphasizing early detection and accurate diagnosis, which is boosting the demand for CT and MRI contrast agents, especially with the growing prevalence of chronic diseases such as cancer, cardiovascular disorders, and neurological conditions. These diseases require detailed imaging for accurate monitoring and treatment planning, further driving the adoption of contrast agents.

Major companies operating in the CT and MRI contrast agents industry are GE HealthCare, Bayer AG, Bracco S.p.A., Guerbet, LLC, Fujifilm Holdings Corporation, Lantheus Holdings, Inc., Boston Scientific Corporation, Slate Run Pharmaceuticals, Shimadzu Corporation, PatSnap, Beijing Beilu Pharmaceutical Co., Ltd., Kohlberg Kravis Roberts & Co. Inc., Spago Nanomedical AB, Koninklijke Philips N.V., and Trivitron Healthcare.

Additionally, the development of innovative contrast agents that are safer, more efficient, and better tolerated by patients is enhancing the overall imaging experience and improving patient outcomes. The introduction of specialized agents, including those enabling functional and molecular imaging, is also driving the market.

Furthermore, the expansion of healthcare infrastructure, especially in emerging economies, is increasing the accessibility of advanced diagnostic imaging services, further supporting market growth. The rising number of diagnostic imaging centers, coupled with a growing preference for non-invasive diagnostic techniques, is also contributing to the upward trajectory of the market.

- In April 2023, GE HealthCare announced the launch of Pixxoscan (gadobutrol), expanding its portfolio of Magnetic Resonance Imaging (MRI) contrast agents. The product, reviewed with a regulatory decentralized procedure, offers an additional option for radiology departments to enhance a broad range of MRI procedures, providing improved diagnostic accuracy and personalized care for patients.

Key Highlights:

- The CT and MRI contrast agents industry size was valued at USD 5.98 billion in 2023.

- The market is projected to grow at a CAGR of 8.70% from 2024 to 2031.

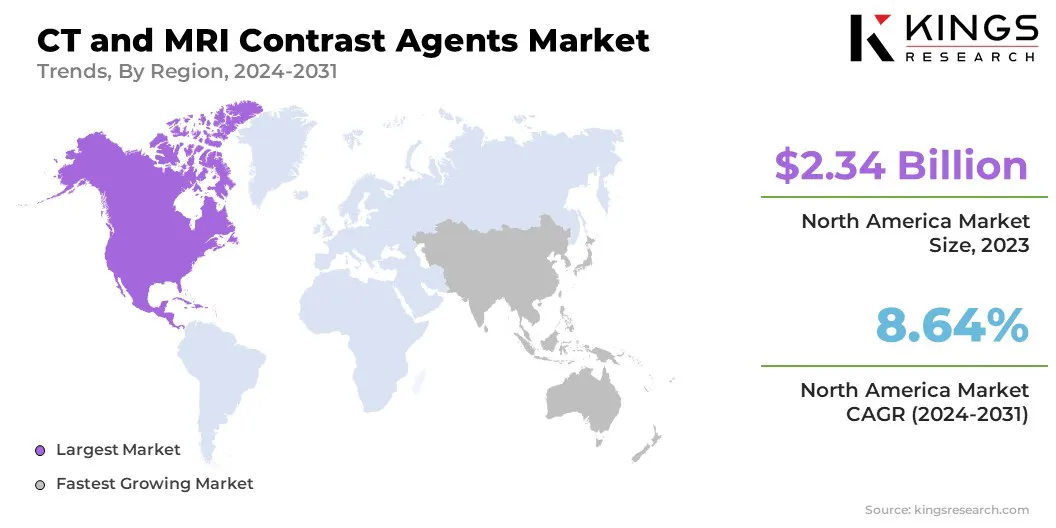

- North America held a market share of 39.17% in 2023, with a valuation of USD 2.34 billion.

- The iodinated contrast media segment garnered USD 3.36 billion in revenue in 2023.

- The X-ray/ computed tomography segment is expected to reach USD 6.95 billion by 2031.

- The cancer segment is expected to reach USD 3.31 billion by 2031.

- The intravenous segment is expected to reach USD 10.11 billion by 2031.

- The hospitals segment is expected to reach USD 7.62 billion by 2031.

- The market in Asia Pacific is anticipated to grow at a CAGR of 9.65% during the forecast period.

Market Driver

Increasing Demand for Early Diagnosis and Screening

The increasing demand for early diagnosis and screening is driving the market. The early detection of diseases such as cancer, cardiovascular disorders, and neurological conditions has become critical as healthcare systems globally shift toward preventive medicine.

Early diagnosis improves treatment outcomes by identifying diseases at an initial, more treatable stage. Contrast agents used in CT and MRI scans enhance the visibility of organs, tissues, and blood vessels, making it easier for doctors to detect abnormalities and monitor disease progression.

Many people are undergoing regular screenings, especially in high-risk populations, which is increasing the demand for these diagnostic tools, and consequently contrast agents. Additionally, technological advancements in imaging systems have significantly enhanced the capabilities of CT and MRI scans, further driving the CT and MRI contrast agents market.

Innovations in imaging technologies, such as high-resolution scanners, improved image processing software, and advanced magnetic field techniques, allow for clearer, more detailed, and accurate images. These advancements help radiologists identify even the smallest abnormalities, improving the overall diagnostic process.

These new technologies are widely adopted in healthcare facilities, boosting the need for more effective and reliable contrast agents to enhance image clarity. This synergy between cutting-edge imaging systems and contrast agents is fostering greater precision in diagnosis and personalized treatment plans, propelling the market.

- In April 2024, Sanochemia Pharmazeutika secured exclusive licensing rights from SPL Medical for Ferrotran, a new MRI contrast agent based on ferumoxtran. The agent, currently in Phase III clinical trials, is designed to detect small lymph node metastases in prostate cancer patients and may be used for other cancer types in the future.

Market Challenge

Safety Concerns Regarding CT and MRI Contrast Agents

A major challenge in the market is the risk of adverse reactions and side effects when using contrast agents, particularly gadolinium-based contrast agents (GBCAs). While these agents are generally safe, they are not without risks. The most notable concerns include allergic reactions, nephrogenic systemic fibrosis (NSF), and gadolinium deposition in the brain and other organs.

NSF is a rare but serious condition, which primarily affects patients with severe renal impairment and can lead to tissue fibrosis, joint stiffness, and other complications. Additionally, recent studies have raised concerns about the long-term accumulation of gadolinium in the body, especially in the brain and in patients with normal kidney function.

This has led to increasing scrutiny from health regulators and a push for safer alternatives. In some cases, these safety concerns cause hesitation among healthcare professionals when deciding whether to use GBCAs, particularly for patients with existing kidney conditions or those requiring repeated imaging.

The development of gadolinium-free contrast agents is being prioritized. These agents are designed to offer the same diagnostic capabilities as traditional GBCAs without the associated risks, reducing the likelihood of adverse reactions.

Market Trend

Gadolinium-free Contrast Agents and the Rise of Personalized Medicine & Tailored Imaging

The development of gadolinium-free contrast agents is a growing trend in the CT and MRI contrast agents market, as concerns about the potential toxicity of GBCAs continue to rise. Gadolinium has been linked to rare but serious side effects, including nephrogenic systemic fibrosis in patients with kidney problems.

As a result, there is a shift toward developing alternative contrast agents that are safer, especially for patients with compromised renal function. Gadolinium-free agents reduce the risks associated with gadolinium while providing effective contrast for high-quality imaging. This trend reflects the industry's commitment to patient safety while improving the overall diagnostic experience.

- In October 2024, GE HealthCare announced the completion of its Phase I clinical trial for a first-of-its-kind macrocyclic manganese-based MRI contrast agent. The trial demonstrated that the agent was well-tolerated with no serious adverse events or clinically relevant findings, positioning it as a potential alternative to gadolinium-based contrast agents. This development aligns with GE HealthCare's commitment to enhancing MRI imaging technology and reducing environmental impact.

Another emerging trend is the growing importance of personalized medicine and tailored imaging. The need for imaging technologies that provide detailed, patient-specific insights is growing as people move toward individualized treatments.

Tailored imaging, facilitated by advanced contrast agents, helps healthcare providers make more precise diagnoses, monitor disease progression, and choose the most effective treatment options.

Personalized medicine is transforming how contrast agents are used in both CT and MRI scans by incorporating genetic, environmental, and lifestyle factors into medical decisions, ensuring that imaging procedures are as specific and effective as possible for each patient.

CT and MRI Contrast Agents Market Report Snapshot

|

Segmentation |

Details |

|

By Product |

Gadolinium-based Contrast Media, Iodinated Contrast Media |

|

By Modality |

Magnetic Resonance Imaging (Elucirem/ Vueway, Dotarem, ProHance, MultiHance, Gadovist, Eovist / Primovist, Clariscan, Other Generics), X-ray/ Computed Tomography (Optiray, ISOVUE, Ultravist, Omnipaque, Visipaque, Other Generics) |

|

By Application |

Cardiovascular Disorders, Neurological Disorders, Gastrointestinal Disorders, Cancer, Nephrological Disorders, Musculoskeletal Disorders, Others |

|

By Route of Administration |

Intravenous, Oral Route, Rectal Route |

|

By End-Use |

Hospitals, Diagnostic Imaging Centers, Others |

|

By Region |

North America: U.S., Canada, Mexico |

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe | |

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific | |

|

Middle East & Africa: Turkey, UAE, Saudi Arabia, South Africa, Rest of Middle East & Africa | |

|

South America: Brazil, Argentina, Rest of South America |

Market Segmentation

- By Product (Gadolinium-based Contrast Media, Iodinated Contrast Media): The iodinated contrast media segment earned USD 3.36 billion in 2023, due to the increasing adoption of CT scans in emergency and diagnostic imaging procedures.

- By Modality (Magnetic Resonance Imaging, X-ray/ Computed Tomography): The X-ray/ computed tomography segment held 58.85% share of the market in 2023, due to the widespread use of CT scans for quick, non-invasive diagnosis of various medical conditions.

- By Application (Cardiovascular Disorders, Neurological Disorders, Gastrointestinal Disorders, Cancer, Nephrological Disorders, Musculoskeletal Disorders, Others): The cancer segment is projected to reach USD 3.31 billion by 2031, owing to the rising incidence of cancer and the growing demand for advanced imaging techniques for early diagnosis and treatment monitoring.

- By Route of Administration (Intravenous, Oral Route, and Rectal Route): The intravenous segment is projected to reach USD 10.11 billion by 2031, owing to its widespread use in both CT and MRI scans for effective contrast enhancement.

- By End-Use (Hospitals, Diagnostic Imaging Centers, Others): The hospitals segment is projected to reach USD 7.62 billion by 2031, owing to the increasing number of hospital-based diagnostic imaging procedures and the demand for advanced imaging technology.

CT and MRI Contrast Agents Market Regional Analysis

Based on region, the market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and Latin America.

North America accounted for 39.17% share of the CT and MRI contrast agents market in 2023, with a valuation of USD 2.34 billion. The dominance of North America can be attributed to several factors, including the high prevalence of chronic diseases such as cancer, cardiovascular disorders, and neurological conditions, which drive the demand for advanced imaging solutions.

Additionally, the presence of well-established healthcare infrastructure, advanced medical technologies, and a high rate of early diagnosis & screening contribute significantly to the market's growth. The adoption of cutting-edge imaging technologies, along with the increasing healthcare spending in the U.S. and Canada, further propels the use of contrast agents in diagnostic imaging.

Moreover, government initiatives and reimbursement policies in North America support the adoption of these technologies, making it the largest contributor to the market.

- In September 2024, Zydus Lifesciences Ltd. announced an exclusive licensing and supply agreement with Viwit Pharmaceuticals for gadobutrol injection and gadoterate meglumine injection, both generic versions of GADAVIST and DOTAREM. The agreement grants Zydus exclusive rights to market, distribute, and sell these Gadolinium-based MRI contrast agents in the U.S. market.

The market in Asia Pacific is expected to register the fastest growth, with a projected CAGR of 9.65% over the forecast period. The rapid expansion of healthcare infrastructure and increased investments in healthcare in countries like China, India, Japan, and South Korea have created strong demand for advanced diagnostic imaging.

Growing awareness about early detection and rising disposable incomes in emerging economies are also driving the demand for contrast agents in the region. Furthermore, the rising incidence of chronic diseases and aging populations in several countries in the region are fueling the market.

The increased focus on modernizing healthcare facilities, along with the development of advanced imaging technologies, is expected to further boost the market. Additionally, the expansion of healthcare access and improvements in diagnostic capabilities in countries like China and India are contributing to the rapid market growth in the region.

Regulatory Frameworks:

- In the U.S., CT and MRI contrast agents are regulated by the U.S. Food and Drug Administration (FDA) under the Federal Food, Drug, and Cosmetic Act. Specifically, these agents are classified as drugs and must undergo a rigorous approval process before being marketed. The FDA's Center for Drug Evaluation and Research (CDER) is responsible for reviewing and approving contrast agents.

- In Europe, CT and MRI contrast agents are regulated by the European Medicines Agency (EMA) under the European Union's (EU) Medicines Directive. These agents must be approved for use as medicinal products by the EMA's Committee for Medicinal Products for Human Use (CHMP).

- In China, CT and MRI contrast agents are regulated by the National Medical Products Administration (NMPA), formerly known as the China Food and Drug Administration (CFDA). The NMPA oversees the approval and monitoring of medical devices and drugs, including contrast agents. Manufacturers must submit clinical trial data to demonstrate the safety, efficacy, and quality of contrast agents.

- In Japan, CT and MRI contrast agents are regulated by the Pharmaceuticals and Medical Devices Agency (PMDA), which operates under the Ministry of Health, Labour and Welfare (MHLW). The approval process includes a comprehensive review of clinical trials, manufacturing practices, and adherence to Good Manufacturing Practices (GMP).

- In India, CT and MRI contrast agents are regulated by the Central Drugs Standard Control Organization (CDSCO) under the Ministry of Health and Family Welfare. The CDSCO is responsible for the approval and monitoring of pharmaceutical products, including diagnostic contrast agents.

Competitive Landscape

The CT and MRI contrast agents industry is characterized by key players focusing on a variety of strategies to maintain and expand their market share. One of the primary strategies employed is extensive Research and Development (R&D) to introduce innovative contrast agents that offer enhanced safety profiles, greater efficiency, and improved patient tolerance.

Companies are increasingly investing in the development of specialized contrast agents that enable advanced imaging techniques, such as molecular and functional imaging, to cater to a broader range of medical conditions.

Strategic partnerships and collaborations also play a significant role in the market, with key players partnering with healthcare providers, research institutions, and imaging centers to expand their product portfolios and distribution networks. Mergers and acquisitions are frequently used to consolidate market positions, enhance technological capabilities, and expand geographical reach.

Furthermore, a strong focus on regulatory compliance and obtaining necessary approvals is critical to ensuring the safety and effectiveness of contrast agents, leading to enhanced credibility and trust in the market. Many players also emphasize regional expansion, particularly in emerging markets, to capitalize on the growing healthcare infrastructure and increasing demand for advanced diagnostic imaging.

- In November 2024, Bracco announced that it would triple the production of its innovative ultrasound contrast agent at a new manufacturing facility in Geneva. The significant investment of over USD 86 million will increase the production of Contrast-Enhanced Ultrasound (CEUS) microbubbles, which enhance diagnostic imaging for heart cavities, blood vessels, and tissue vascularity.

List of Key Companies in CT and MRI Contrast Agents Market:

- GE HealthCare

- Bayer AG

- Bracco S.p.A.

- Guerbet, LLC

- Fujifilm Holdings Corporation

- Lantheus Holdings, Inc.

- Boston Scientific Corporation

- Slate Run Pharmaceuticals

- Shimadzu Corporation

- PatSnap

- Beijing Beilu Pharmaceutical Co., Ltd.

- Kohlberg Kravis Roberts & Co. Inc.

- Spago Nanomedical AB

- Koninklijke Philips N.V.

- Trivitron Healthcare

Recent Developments (M&A/Partnerships/Agreements/Product Launch)

- In January 2025, Bayer announced positive topline results from the pivotal Phase III QUANTI studies evaluating the investigational GBCA gadoquatrane. The studies demonstrated that gadoquatrane effectively met primary and secondary efficacy endpoints at a 60% lower gadolinium dose compared to traditional macrocyclic GBCAs, showcasing its potential for safer and more efficient MRI imaging.

- In April 2024, Guerbet announced the first administration of Elucirem (Gadopiclenol), a new macrocyclic gadolinium-based contrast agent, to European patients undergoing MRI scans. Elucirem offers high relaxivity and requires half the gadolinium dose compared to other contrast agents, addressing concerns regarding gadolinium exposure, particularly for patients needing multiple MRI exams.